Warren Buffett recently released his Berkshire Hathaway Annual Report 2019. One of the key take-aways from the letter is Berkshire’s ongoing focus on the power of retained earnings from the companies in which Berkshire invests. Here’s an excerpt from the letter:

At Berkshire, Charlie and I have long focused on using retained earnings advantageously. Sometimes this job has been easy – at other times, more than difficult, particularly when we began working with huge and evergrowing sums of money.

In our deployment of the funds we retain, we first seek to invest in the many and diverse businesses we already own. During the past decade, Berkshire’s depreciation charges have aggregated $65 billion whereas the company’s internal investments in property, plant and equipment have totaled $121 billion. Reinvestment in productive operational assets will forever remain our top priority.

In addition, we constantly seek to buy new businesses that meet three criteria. First, they must earn good returns on the net tangible capital required in their operation. Second, they must be run by able and honest managers. Finally, they must be available at a sensible price.

When we spot such businesses, our preference would be to buy 100% of them. But the opportunities to make major acquisitions possessing our required attributes are rare. Far more often, a fickle stock market serves up opportunities for us to buy large, but non-controlling, positions in publicly-traded companies that meet our standards.

Whichever way we go – controlled companies or only a major stake by way of the stock market – Berkshire’s financial results from the commitment will in large part be determined by the future earnings of the business we have purchased. Nonetheless, there is between the two investment approaches a hugely important accounting difference, essential for you to understand.

In our controlled companies, (defined as those in which Berkshire owns more than 50% of the shares), the earnings of each business flow directly into the operating earnings that we report to you. What you see is what you get.

In the non-controlled companies, in which we own marketable stocks, only the dividends that Berkshire receives are recorded in the operating earnings we report. The retained earnings? They’re working hard and creating much added value, but not in a way that deposits those gains directly into Berkshire’s reported earnings. At almost all major companies other than Berkshire, investors would not find what we’ll call this “nonrecognition of earnings” important. For us, however, it is a standout omission, of a magnitude that we lay out for you below.

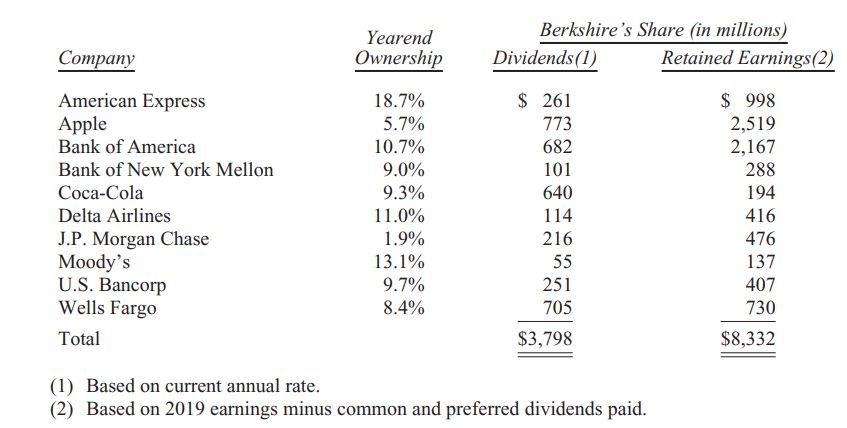

Here, we list our 10 largest stock-market holdings of businesses. The list distinguishes between their earnings that are reported to you under GAAP accounting – these are the dividends Berkshire receives from those 10 investees – and our share, so to speak, of the earnings the investees retain and put to work. Normally, those companies use retained earnings to expand their business and increase its efficiency. Or sometimes they use those funds to repurchase significant portions of their own stock, an act that enlarges Berkshire’s share of the company’s future earnings.

Obviously, the realized gains we will eventually record from partially owning each of these companies will not neatly correspond to “our” share of their retained earnings. Sometimes, alas, retentions produce nothing. But both logic and our past experience indicate that from the group we will realize capital gains at least equal to – and probably better than – the earnings of ours that they retained. (When we sell shares and realize gains, we will pay income tax on the gain at whatever rate then prevails. Currently, the federal rate is 21%.)

It is certain that Berkshire’s rewards from these 10 companies, as well as those from our many other equity holdings, will manifest themselves in a highly irregular manner. Periodically, there will be losses, sometimes company-specific, sometimes linked to stock-market swoons. At other times – last year was one of those – our gain will be outsized. Overall, the retained earnings of our investees are certain to be of major importance in the growth of Berkshire’s value.

Mr. Smith got it right.

You can find a copy of the BRK Annual Report here: Berkshire Hathaway Annual Report 2019.

Related articles:

Here’s How Charlie And Warren Calculate Intrinsic Value Differently To Everyone Else

Warren Buffett: “The Worst Deal That I’ve Made”

For all the latest news and podcasts, join our free newsletter here.

Don’t forget to check out our FREE Large Cap 1000 – Stock Screener, here at The Acquirer’s Multiple: