We’ve updated the look and functionality of the screeners.

Functionality

These are the material changes to functionality:

- Financials and Utilities: We’re including the Financials and Utilities sectors for the first time. To accommodate the new sectors, we’re making two additional changes.

- Expanding Number of Stocks: We’re expanding the number of stocks visible to the full dataset in the paid screeners. To increase the diversification of the screens, we’re showing the best six (6) opportunities in each industry. (If we don’t limit the opportunities to the top six in each category, there are too many stocks from some industries, particularly in the Financials sector, for example United States Banks, Investment Services, Specialty Finance and Insurance).

- Market Cap Cut-Off: We’re also increasing the Large Cap minimum market cap to $20 billion (The All Investable / Small and Micro cut-off is approximately $2 billion.)

Appearance

We’re also changing the look of the screeners to include some additional charts, downloadable tables, and four (4) additional metrics:

- ROA (%): Five-year average operating income return on total assets. This shows the historical earning power of a stock’s assets.

- Incremental Growth (%): This is the reinvestment rate (capital expenditures less depreciation divided by total assets) multiplied by ROA. It can be positive–if cap ex exceeds depreciation–or negative–if cap ex falls short of depreciation. Companies with a high reinvestment rate and a high ROA will score higher on the Incremental Growth metric. Low or negative reinvestment rates and a low ROA will score lower on the Incremental Growth metric.

- Expected Return (%): This is a variation on Bruce Greenwald’s Expected Return calculation. It is calculated by summing Earning Power, Incremental Growth and Shareholder Yield.

- IV/P (%): Implied Value to Price (IV/P). IV/P is calculated by taking the value of the Expected Return implied for each stock by dividing it by the ten-year treasury yield and comparing it to the stock price. Numbers greater than 1 indicate more Implied Valued than Price. Think of it as an estimate of the value offered for each dollar invested.

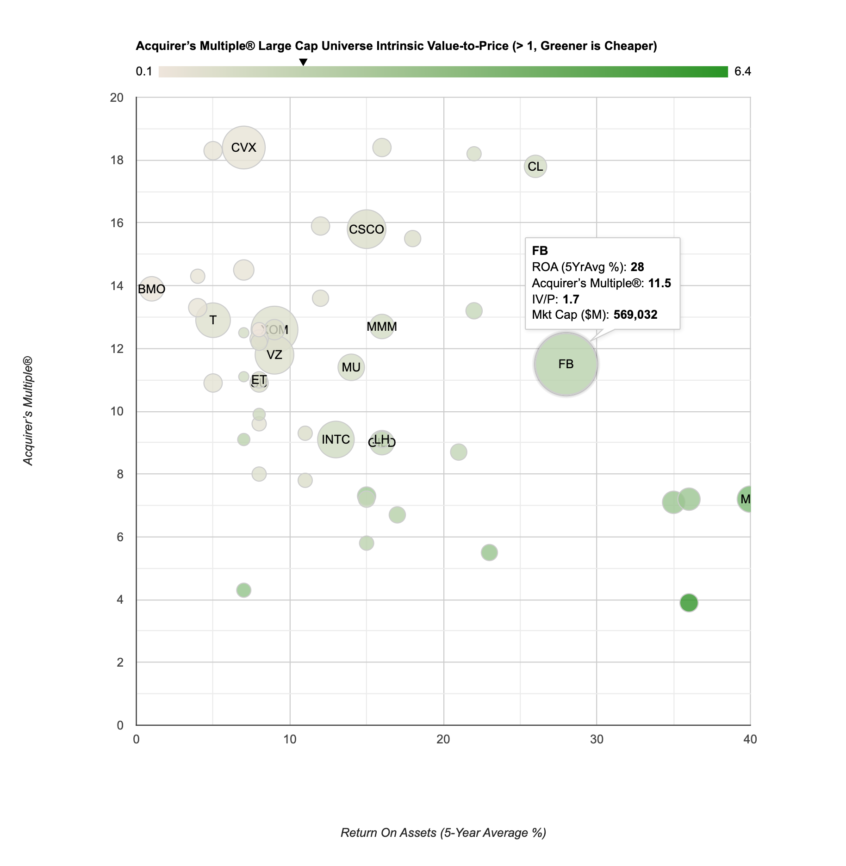

Bubble Charts

Finally, we’re adding bubble charts like the one above to each screen showing the Acquirers Multiple on one axis and ROA on another. Bigger bubbles are bigger stocks with bigger market caps, and vice versa. The bubble chart is color-coded–green indicates a higher-than-average IV/P and better value, red indicates a lower-than-average IV/P and worse value. Hovering over a bubble shows the details of each stock.

Using the Screeners

The four additional columns (ROA, Incremental Growth, E(r) and IV/P) give us some additional flexibility with the screeners. The screens can be used to find different investment ideas based on different investment styles. Rank on Acquirers Multiple, FCF Yield, IV/P (Implied Value / Price), Expected Return, Incremental Growth, Shareholder Yield, Buyback Yield, Dividend Yield, ROA (Return on Assets),

Here’s how they work:

- Acquirers Multiple: Ranking on this column shows the stocks with the lowest multiples in the universes. These are deep value stocks that may benefit from mean reversion in the underlying businesses. This is the traditional deep value screen.

- FCF Yield or Free Cash Flow Yield: Trailing Twelve-Month Free Cash Flow divided by Market Capitalization. Another traditional deep value screen. These stocks benefit from mean reversion in fundamentals and multiples.

- ROA or Return on Assets: Ranking on this column shows the stocks with the highest five-year average operating income returns on total assets. These are the most profitable companies in the universes over the last five years.

- Incremental Growth (%): Incremental Growth shows stocks with the highest sustainable growth rates over the last five years.

- E(r) or Expected Return (%): The sum of a stock’s Earning Power, Incremental Growth and Shareholder Yield. This is a variation of Bruce Greenwald’s calculation. It assumes no mean reversion in multiples or fundamentals.

- IV/P or Intrinsic Value to Price: This column compares the stock’s Implied Value (Earning Power, Incremental Growth plus Shareholder Yield)to the current price. The number represents the value offered for each dollar invested. IV/P greater than one (1) indicates that each dollar invested receives more than $1 of Intrinsic Value. IV/P less than one indicates less than $1 of Intrinsic Value for each dollar invested. The IV/P is necessarily a rough estimate. These stocks benefit from mean reversion in multiples, and no mean reversion in fundamentals. Where the market is applying a lower Acquirers Multiple to a stock’s Expected Return, it may indicate an undervalued opportunity. This is a profitability-at-a-reasonable price screen. Historically, getting more an IV/P lower than about 0.6–each dollar invested buys 60 cents or less of Intrinsic Value–is overvalued.

-

Buyback Yield, Dividend Yield, and Shareholder Yield show the stocks with the highest payout ratios.

As always, we exclude from the universe companies with the worst Beneish, Piotroski and Altman scores, and the most heavily shorted stocks.

Let us know what you think!

Definitions

- IV/P is Implied Value to Price. Any IV/P greater than one (1) might indicate the stock offers more than $1 of intrinsic value for each $1 of the stock price. IV/P lower than one (1) might indicate the stock offers less than $1 of intrinsic value for each $1 of the stock price.

- Implied Value converts Expected Return into a value. It is the sum of the value of each stock’s Earning Power, Incremental Growth and Shareholder Yield.

- Expected Return is Earning Power plus Incremental Growth plus Shareholder Yield

- Earning Power is a stock’s Return on Assets. To find the value we assume a perpetuity divided by the current Ten (10)-year Treasury Yield

- Return on Assets is the five (5)-year average Operating Income divided by Total Assets.

- Incremental Growth is the Reinvestment Rate multiplied by Return on Assets. It can be positive or negative. To find the value we assume a perpetuity divided by the current Ten (10)-year Treasury Yield

- Reinvestment Rate is the five (5)-year average of Capital Expenditures minus Depreciation divided by Total Assets. A negative figure indicates Depreciation exceeds Capital Expenditure. A positive figure indicates Capital Expenditure exceeds Depreciation.

- Shareholder Yield is the sum of a stock’s Buyback Yield and Dividend Yield. To find the value we assume a perpetuity divided by the current Ten (10)-year Treasury Yield

- Dividend Yield is the five (5)-year average Dividend divided by the Market Capitalization.

- Buyback Yield is the five (5)-year average Net Equity Repurchased (Equity Issued minus Equity Repurchased) divided by Market Capitalization

For all the latest news and podcasts, join our free newsletter here.

Don’t forget to check out our FREE Large Cap 1000 – Stock Screener, here at The Acquirer’s Multiple:

15 Comments on “Updates to the Screeners”

Hi,

After this update, would you suggest to continue focusing on buying the 30 stock with lowers Acquirer’s Multiple no matter the industry? Or should we change how we follow the methodology?

Keep following the screen. The cheapest 30 from the screen will give industry diversification.

Can you please explain how the debt to equity ratio shown in the screens can be negative? Are you subtracting cash from the debt?

Yes, net cash.

Is there any reason why you increased the Market Cap to $20 Billion of the Large Cap Screener? Is this because of the 50th percentile and companies are worth more now? Because I noticed couple days ago that stocks like $ZIM and $TX were in the Screener and had extremely low AM’s. Now with this update all the AM seem higher.

Thanks in advance 🙂

Yes, the screens haven’t kept up with the increase in market caps. ZIM and TX are in the All Investable.

Personally I’d be interested in the MOST shorted stocks that also appear cheap on a value basis – though I admit I don’t know what the data says about how that would perform vs a basket of companies that aren’t heavily shorted.

Interesting idea. They tend to underperform pretty consistently. Shorts are smart.

I am a fellow investor from Germany I am following you for a long time and

Thanks for your efforts to improve the screens but I have two concerns:

Firstly ,I really don’t like the idea to increase market caps of each screeners. Although we will get less volatile portfolios , it is going to badly hurt ROI of each screens as a portfolio . Especially,compare to previous market caps limits .Is there any new research about this recent marek cap cut-off changes impact on ROI.

Secondly , as far as I know that extensive research ( you present in your book´´the Acquirer ´s Multiple ´´ and also in the Greenblatt´s Magic Formula) does not include any financial and utility firms intentionally and suddenly you decided to include financials and utilities which are another world with entirely different measures and dangers ? Is there any back tested research about financials and utilities ` performance in Acquirer`s Multiple portfolio ?

The screens haven’t kept up with the increase in market caps. I’ve had requests to include Financials and Utilities and I don’t want to exclude any sectors I would otherwise invest in. The additional metrics can be used for Financials and Utilities. If you don’t wish to use them, feel free to avoid them.

Can you explain why you decided to include financials and utilities? Also, is there anything to suggest what could be a “tie breaker” in the event of two companies having the same AM/multiple? (e.g. looking at and ranking the next best metric after the AM)?

I’ve had requests to include them and I don’t want to exclude any sectors I would otherwise invest in. The additional metrics can be used for Financials and Utilities. If you don’t wish to use them, feel free to avoid them. Secondary metrics include E(r), ROA, IV/P, FCF Yield. All are useful.

“We exclude utilities and financials because they have unusual financial statements that don’t readily fit an analysis using the acquirer’s multiple.” Would it be possible to maybe get a blog post or a bit more information on adding these industries in? I’m not opposed at all – I just want to understand why the change outside of requests to do so. E.g did you back test the updated AM and what were the results? Not trolling, looking to learn 🙂

Hi Tobias,

I just finished reading the book and have searched the website a bit, but I can’t see a part about when to sell the stocks. How do you work out when the stock has reverted to the mean?

Hey Steven. You can find the strategy for selling a stock here:

https://acquirersmultiple.com/2016/04/four-steps-to-implementing-a-quantitative-value-investment-strategy/