One of the investors we like to follow closely here at The Acquirer’s Multiple is Chuck Royce and his team at The Royce Funds. The Royce Funds recently released their commentary (see video below) on the success that they’re having with their deep value investing strategy using Enterprise Value to EBIT as a valuation metric saying:

“If you look at the overall Russell 2000 and say what are the bottom three deciles on valuation, using enterprise value to earnings before interest and taxes as the valuation metric, what you find is there’s a wide variation. That the bottom three deciles sell between a 28% to 57% discount to the overall market. The small-cap market is so wide and diverse that while still maintaining the valuation discipline, the Opportunity Strategy is always finding interesting investment candidates.”

Here’s an excerpt from that commentary:

How would you describe Royce’s Deep Value Strategy to an asset allocator?

So we characterize the Royce Opportunity Strategy as a deep value strategy. Why do we do that? Well, valuation is really at the core of the discipline, in that they, they look for stocks that are cheap based on price-to-book and price-to-sales. Actually distinctively cheap. Generally 25 to 30% cheaper than the overall market. You know, that creates a portfolio that has a number of attributes. The first is, it has high active share. So it regularly is 90 or above active share portfolio. The second is, a distinctive portfolio has the opportunity for distinctive performance. And this strategy has a history of that. Over 70% of the rolling five-year periods, the strategy has beaten the Russell 2000.

How has the Fund performed in single digit market environments?

We think that’s a particularly relevant question because at Royce we believe we are transitioning from a period where the small-cap index, the asset class itself, gave you double digit returns, to a period which is probably more likely to be single digit. Let’s look at Opportunity Strategy and how it has executed in those different environments.

Monthly Rolling 5-Year Average Excess Returns

Opportunity Minus Russell 2000 from 11/30/96 through 6/30/18

Russell 2000 Five-Year Return Range

Well, the history is that the greatest spread on rolling five-year basis that Opportunity Strategy has had has actually been in single digit return environments for the Russell 2000. More precisely when returns have been on a five-year basis between 5 and 10% for the Russell, that has been actually the best spread period for the Opportunity Strategy. Why is that relevant now? Well, we think the most likely scenario for the next five years is that high single digit return for small-caps, and historically that’s been really good for this strategy.

How has the strategy historically done in rising interest rate environments?

We think perhaps among the most underappreciated attributes of the Royce Opportunity Strategy is how well it has historically done in rising interest rate environments.

When 10-Year Treasury Yield was Rising, Opportunity Outperformed the Russell 2000

Trailing Monthly Rolling 1-Year Returns (11/30/96-6/30/18)

The performance data and trends outlined in this video are presented for illustrative purposes only. Past performance is no guarantee of future results. Historical market trends are not necessarily indicative of future market movements.

So if you look one year periods where the 10-year treasury yield has risen over the course of that period, and you said, “How did Opportunity Strategy do versus the small-cap index,” the striking result is over 90% of those periods Opportunity beat the Russell 2000 and by an average of over 1,100 basis points. So rising interest rate environments, if that’s what an allocator thinks is coming, this strategy has historically done quite well.

What is the case for investing in Opportunity strategy today?

So a reasonable question may be well, markets are at all-time highs, you probably are having a hard time finding attractive investments. Maybe this isn’t the best time for this strategy. So that perspective, we think reveals what we think is an enduring misunderstanding about the small-cap market. So one of the things that we feel is perennially underappreciated about the small-cap market is that cliché that it’s, it’s not a stock market, it’s a market of stocks. And what we mean by that is there is wide variation in both quality and valuation at all times and that creates opportunity.

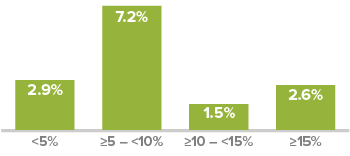

Many Small-Caps Sell at a Significant Discount

Bottom Three Deciles in Russell 2000 Median

LTM EV/EBIT 1 ex negative EBIT as of 6/30/18

1Last Twelve Months Enterprise Value/Earnings Before Interest and Taxes

If you look at the overall Russell 2000 and say what are the bottom three deciles on valuation, using enterprise value to earnings before interest and taxes as the valuation metric, what you find is there’s a wide variation. That the bottom three deciles sell between a 28 to 57% discount to the overall market. The small-cap market is so wide and diverse that while still maintaining the valuation discipline, the Opportunity Strategy is always finding interesting investment candidates.

Here’s the commentary video:

For all the latest news and podcasts, join our free newsletter here.

Don’t forget to check out our FREE Large Cap 1000 – Stock Screener, here at The Acquirer’s Multiple:

One Comment on “Chuck Royce: Deep Value Investing Using Enterprise Value To EBIT As A Valuation Metric”

The Operating Earnings used to calculate the Acquirer’s Multiple is calculated from the top line down. How does it differ from EBIT? Is there a standard way to calculate EBIT?