Alliance Resource Partners is a producer and marketer of coal in the United States. The firm operates twelve underground mining complexes in Illinois, Indiana, Kentucky, Maryland and West Virginia. The mining operations are near major power plants. This favorable geographic location helps to minimize costs for customers. It is an important competitive advantage in my opinion. Despite the collapse in the coal price, Alliance Resource continues to generate strong cash flows.

In fact, coal is probably the most hated commodity at the moment. The coal shipped from the Australian port of Newcastle is selling around $55 per tonne. That is the lowest level since 2007. Clearly, many producers are feeling the pain and this is a good news. Walter Energy, Alpha Natural Resources and Patriot Coal went bankrupt in the past few months. Moreover, Arch Coal is almost game over with a market capitalization of $55 million and a huge debt load of $5 billion. The situation is similar for the giant Peabody Energy. In brief, the best cure for low coal prices is low coal prices. These bankruptcies are a good news.

Glencore, the world’s biggest exporter of coal, cut production by about 15% this year. Teck Resources, one of the Canada’s largest mining companies also reduced its output by a meaningful amount. These cuts are widespread in the coal industry. At the moment, the outlook for coal stock is disgusting. Coal companies are hated to death and this is the main reason why I like Alliance Resource Partners. In my opinion, it is an excellent contrarian opportunity.

Actually, its balance sheet is probably the most robust versus any other player in the industry. With current assets of $378 million and current liabilities of $229 million, it is possible to calculate a working capital of $149 million. This is reassuring. With an equity figure of $1,050 million and total liabilities of $1,280 million, the debt to equity ratio is 1.22. For example, Peabody Energy has a debt to equity ratio of 6.17. This metric is equal to 4.76 for Arch Coal. In brief, Alliance Resource Partners has a solid balance sheet and the bankruptcy risk is non-existent.

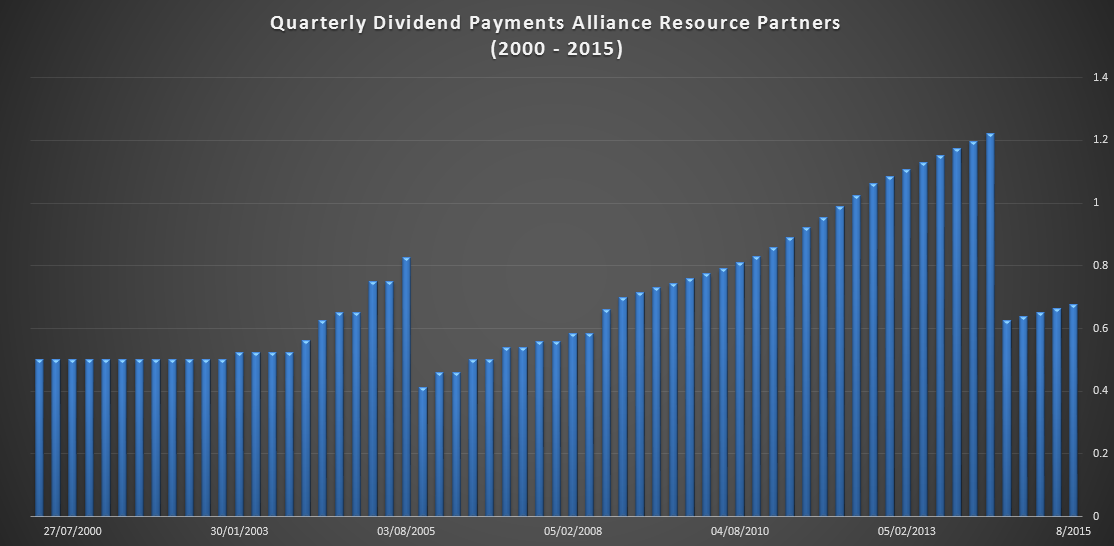

Furthermore, the firm is profitable quarter after quarter despite the record low coal price. On a trailing twelve months basis, the firm generated $510 million in operating income. Based on an enterprise value of $2,416 million, the acquirer’s multiple is equal to 4.74. Without a doubt, it is very low. I want to mention that the firm generated $438.12 million in free cash flow over the last twelve months. It is important to remember that prices are at a record low-level. With a market capitalization of $1,600 million, the free cash flow yield is equal to 27.38%. Likewise, the firm pays a quarterly dividend of $0.675. According to the actual stock price of $21.71, the dividend yield is 12.4%. At the first look, it seems unsustainable. However, the payout ratio is manageable at 88%.

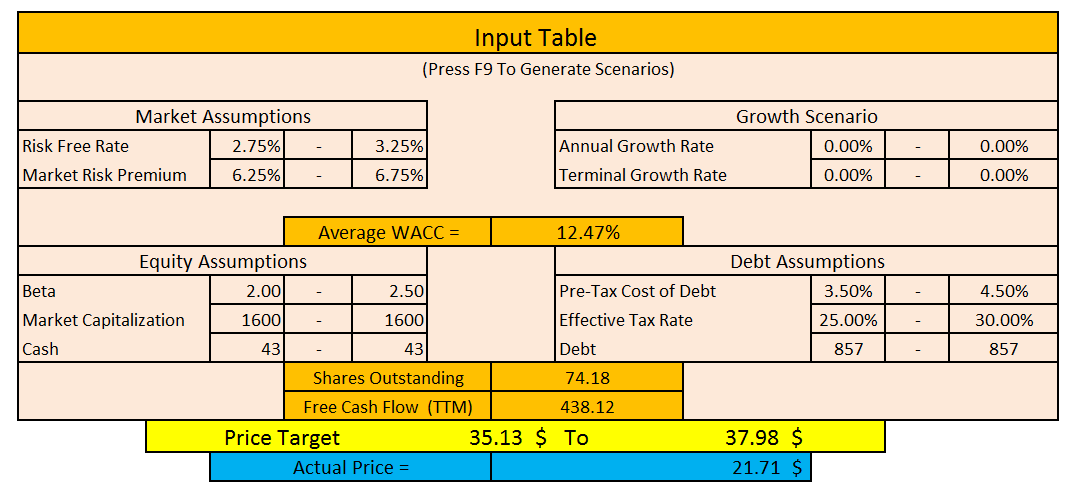

Finally, a discounted cash flow analysis corroborates my entire thesis. I used a worst case scenario. Indeed, an annual growth rate and a terminal growth rate of 0% is almost impossible. One day, coal prices will rebound in my opinion. It is the nature of any commodities. According to many financial websites, the beta of Alliance Resource Partners is around 0.9. To be conservative, I used a beta between 2 and 2.5. The complete input table is illustrated below.

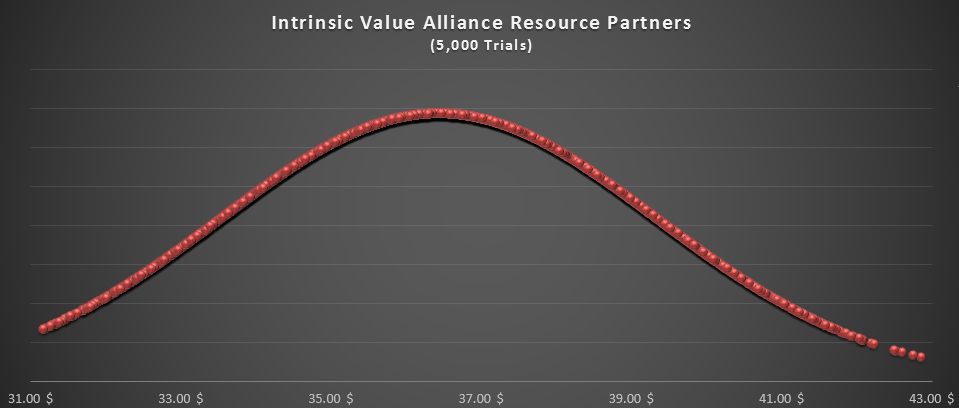

According to my model, the intrinsic value of Alliance Resource Partners is between $35.13 and $37.98. Currently, the stock is trading around $22. Every metric looks cheap. The price to earnings ratio is equal to 5.5 and the EV/EBITDA ratio is extremely low at 3.10. The graph below illustrates the intrinsic value distribution based on 5,000 different scenarios.

In conclusion, Alliance Resource Partners is a diamond in the rough. The coal industry is ugly and disgusting, but ARLP is definitely worth a look at the current price. With its healthy balance sheet, the firm is well positioned to weather the current crisis in the coal industry. Due to record low coal prices, the downside seems limited. Indeed, stocks are not cheap and popular at the same time.

I am an undergraduate student, not a professional. Please take this factor into consideration. Despite the bearish tone of my article, please do your own due diligence and consult your financial advisor before taking any action. I am not a financial advisor. This article expresses my own opinion only. The opinions in this document are for informational and educational purposes only and should not be construed as a recommendation to buy or sell the stocks mentioned. The information in this document is believed to be accurate, but under no circumstances should a person act upon the information contained within. We do not recommend that anyone acts upon any investment information without first consulting an investment advisor as to the suitability of such investments for his specific situation.

For all the latest news and podcasts, join our free newsletter here.

Don’t forget to check out our FREE Large Cap 1000 – Stock Screener, here at The Acquirer’s Multiple:

One Comment on “Alliance Resource Partners, L.P. A Diamond In The Rough $ARLP”

Pingback: Understanding Alliance Resource Partners ($ARLP): A deeply undervalued and overlooked company | The Acquirer’s Multiple®