Valero Energy Corporation ($VLO), which at one point was the cheapest stock in the Large Cap 1000 Screener and the All Investable Screener, is having a blockbuster year, up 33 percent to date (I’ve been pitching it since September last year, here with Jeff Macke on Yahoo Finance). Even so, the business continues to improve at a rapid rate and it continues to be the second cheapest name in the Large Cap 1000 Screener and the seventh cheapest name in the All Investable Screener. That might be because, unlike the usual stocks covered here, it’s carrying net debt to the tune of $2.2 billion. With its $33 billion market cap, the debt pushes the enterprise value to $35.2 billion. It earned $7 billion in operating earnings last year, putting it on an acquirer’s multiple of 5x. Its PE ratio is just 7.5x. It earned free cash flow / enterprise value of 7 percent, which supports a 1 percent dividend yield and a 4.1 percent buyback yield for a fat 5.9 percent shareholder yield.

With a net debt position, its safety is worth examining in detail. The news there is good: it’s plenty safe. VLO is financially strong, with an F-Score of 7/9 (it falls down on asset turnover–revs/total assets–which fell year-on-year from 3x to 2.5x, and gearing–long-term debt/average assets–which increased from 12 percent to 15 percent). Its Z-Score of 4.75 puts it well into the safe zone away from financial distress (north of 2.99 is considered safe), and VLO’s M-Score of -3.14 means that it’s not a manipulator (anything under -2.22 is good news).

Valero is generating strong free cash flow (ttm price to free cash flow is very low at 12.93) and returns value to its shareholders. Joe Gorder, Valero’s Chairman, emphasized in the latest quarter report that the company continues to focus on its key priorities of optimizing its operations, generating strong results, and returning cash to stockholders. In fact, Valero increased its targeted total payout ratio to approximately 75% of 2015 net income from the previous target of 50%. The company defines total payout ratio as the sum of dividends plus stock buybacks divided by net income from continuing operations attributable to Valero stockholders. Valero returned a total of $870 million in cash to stockholders in the second quarter of 2015, of which $203 million was paid in dividends and $667 million was used to purchase 11.3 million shares of Valero common stock. According to its latest price, the forward annual dividend yield is at 2.44% and the payout ratio only 16.6%. The annual rate of dividend growth over the past three years was very high at 51.8%, over the past five years was at 11.8%, and over the past 10 years was very high at 21.8%.

VLO Dividend data by YCharts

In my previous article about Valero from May 13, I argued that the retreat in its stock price offered an excellent opportunity to buy the stock at a cheap price. Meanwhile, since then the stock has gained 14%. However, Valero’s fundamentals look even better now, and, in my opinion, shares could go much higher.

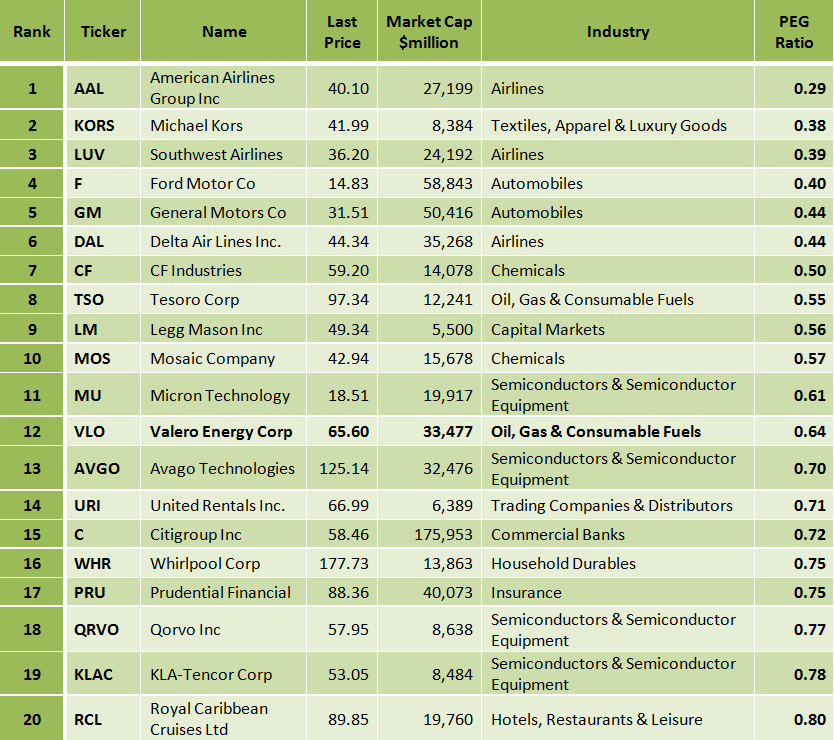

Arie sees it as “extremely undervalued:”

Regarding its valuation metrics VLO’s stock is extremely undervalued. The trailing P/E is very low at 9.15, and the forward P/E is also very low at 10.03. The price-to-sales ratio is extremely low at 0.27, and the enterprise value/EBITDA ratio is very low at 4.64, Moreover, its PEG ratio is also very low at 0.64, the 12th lowest among all S&P 500 companies.

Source: Portfolio123

The PEG Ratio – price/earnings to growth ratio is a widely used indicator of a stock’s potential value. It is favored by many investors over the P/E ratio because it also accounts for growth. A lower PEG means that the stock is more undervalued.

Despite a very good year-to-date, VLO remains one of the cheapest stocks in the screeners. Arie notes that, “[a]ccording to TipRanks, the average target price of the top analysts is at $93, 42% up from its July 28 closing price.” It’s also a safe stock, passing all the metrics I like to examine.

Read more: Valero Energy Continues To Surprise – Valero Energy Corporation (NYSE:VLO) | Seeking Alpha

For all the latest news and podcasts, join our free newsletter here.

Don’t forget to check out our FREE Large Cap 1000 – Stock Screener, here at The Acquirer’s Multiple: