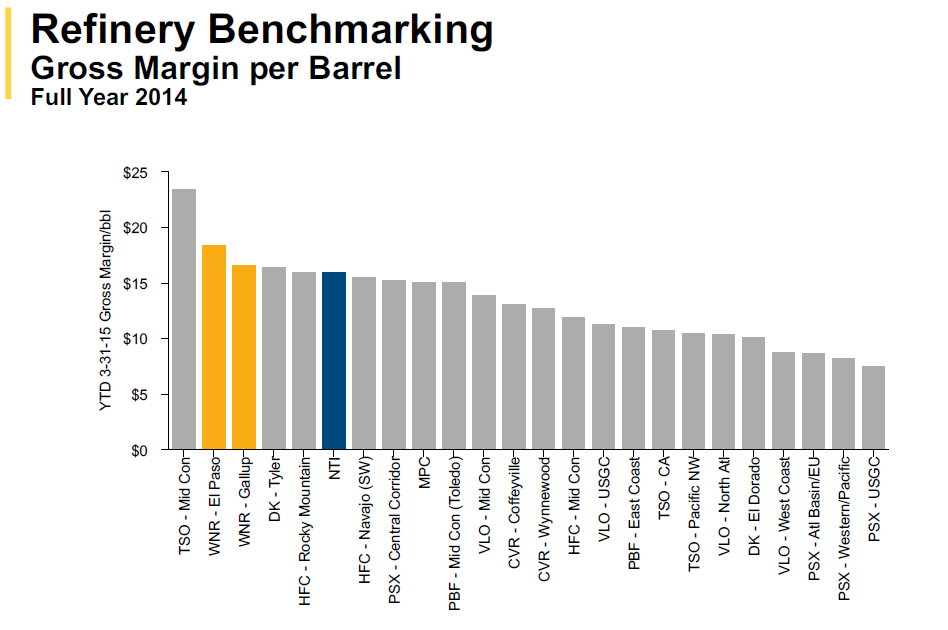

- Western Refining enjoys some of the highest margins in the industry.

- Low leverage, cash generating machine trading at a discount to peers.

- Management committed to shareholder returns – great yield, hefty share repurchases, special dividends.Western Refining (NYSE:WNR) has put itself in a solid position lately but has not seen much love from the broader market which I feel is a bit undeserved.

What does it do?

The company operates in a highly advantaged position that is simply not being reflected by the market and I think it deserves a little bit more love. The company’s operations are simple: it buys oil (most of it domestically produced, in many cases shipping along pipelines it has ownership interest in), refines it into crude-derived products like gasoline, which it then can sell through its own wholesale fuel distribution and retail network. Outside of actually finding and drilling for oil, Western Refining has stakes in the entire chain of events up to the point you squeeze your finger on the gas pump to fill your vehicle. This gives the company almost complete control over one of the most demanded goods that Americans buy.

It’s unloved because it’s a little complex:

To complicate things, much like many other operators in the space, the company has made use of tax-advantaged MLPs. The company owns a 38.4% interest in Northern Tier Energy LP (NYSE:NTI) and a 66.2% interest in Western Refining Logistics (NYSE:WNRL). Through its NTI ownership, it shares an interest in the company’s refining facility in Minnesota and NTI’s retail-marketing network of 254 convenience stores. WNR spun off assets into WNRL (a MLP) in 2013 to split off its storage tank/pipeline business and sold its wholesale operations to WNRL in 2014. Western Refining is Western Refining Logistic’s primary customer.

…

What ties this whole conglomeration together and makes it all extremely attractive is the company’s three refineries and certain advantages they enjoy (these are located in El Paso, Gallup, and St. Paul). The El Paso, Texas location sits near the Permian Basin, long a hotbed for United States domestic production. El Paso is a big hub for pipelines leaving the Permian, and Western Refining takes full advantage. In addition, the company’s own pipeline assets run between the San Juan Basin (which feeds the Gallup, New Mexico refinery) southeast to the Permian Basin, helping link both of these refinery locations together.

…

All of these advantages have led Western Refining to have one of the highest gross margins in the refining business.

Where’s the value:

Recently boosted, Western Refining’s approximate 3% dividend yield is nothing to sneeze at. The company’s $1.36 annual dividend is easily covered by free cash flow (current payout ratio of 52%), leading me to view it as fairly stable even if the company’s business is materially impacted. For those who love free handouts, the company is also prone to throwing special dividends to shareholders – In 2012 the company handed out a $2.50 special dividend and another $2.00 special dividend in 2014. Share repurchases are also common – the company bought back almost 6.5M shares in 2014 for $260M, retiring a sizeable piece of the company’s float. All this led to a staggering $553M being returned to shareholders in 2014.

Given management commentary, we may see another 2015 special dividend if the markets remain strong:

“We’ve said we want to keep about $300 million of cash on the balance sheet, and then at the end of the year we’ll look at returning any excess cash at the end of the year through a special dividend.”

– Jeff Stevens, CEO, Q1 2015 Conference Call

With free cash flow predicted to be healthy all throughout 2015 and with $463M in cash on the balance sheet at the end of Q1, another special dividend isn’t out of the question.

Read more at Western Refining – Unjustly Cheap – Western Refining, Inc. (NYSE:WNR) | Seeking Alpha

For all the latest news and podcasts, join our free newsletter here.

Don’t forget to check out our FREE Large Cap 1000 – Stock Screener, here at The Acquirer’s Multiple: