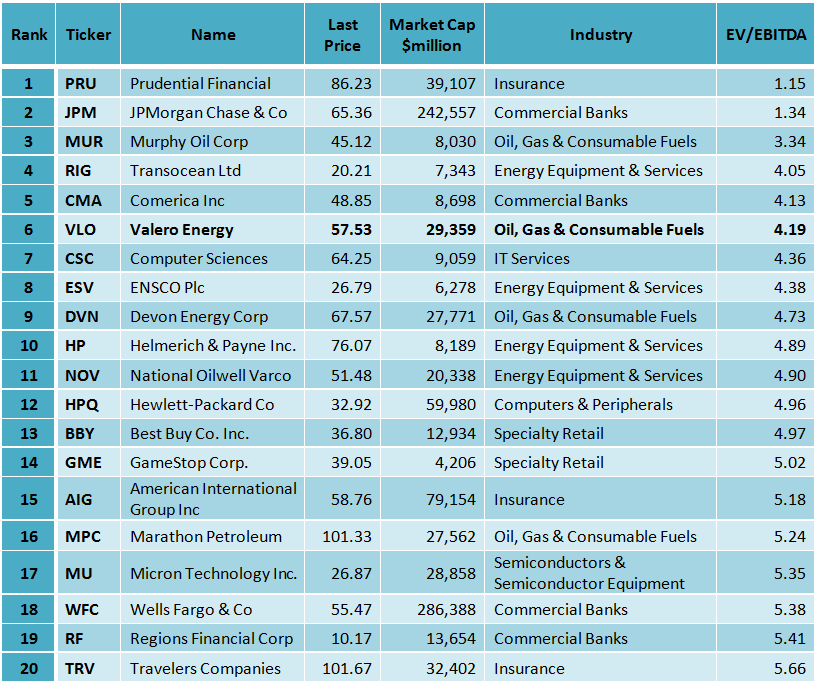

Valero Energy Corporation (NYSE:VLO) is the cheapest stock in the Acquirer’s Multiple Large Cap 1000 screener. Like AGX, it’s another stock that I’ve been pitching for six months (here I am pitching it to Jeff Macke as a takeover target last year). While it’s up more than +22 percent since, it remains an incredibly cheap large cap stock, trading on an acquirer’s multiple of 5.7. It’s also disciplined with its capital allocation and returning cash to shareholders through dividends and a buyback. Arie Goren likes it too. Here’s his rational:

Summary

- Valero delivered strong results for the first quarter of 2015 which were a record first quarter for the company.

- According to my calculation, I see better margin in the current quarter for the refining and the ethanol production compared to the first quarter. Therefore, I anticipate a higher profit for Valero in the second quarter. The company will continue to benefit from lower crude feedstock costs, and from cheap natural gas as an energy source.

- Valero has compelling valuation metrics and strong earnings growth prospects; its Enterprise Value/EBITDA ratio is extremely low at 4.19, and its PEG ratio is also exceptionally low at 0.56. In addition, Valero is generating substantial cash flows and returns value to its shareholders by stock buyback and increasing dividend payments.

- VLO’s stock has retreated 10.8% from its 52 week high; that offers an excellent opportunity to buy the stock at a cheap price.

Valuation

Valero’s valuation metrics are excellent. The trailing P/E is very low at 7.88, the forward P/E is also very low at 9.42, and its price-to-sales ratio is extremely low at 0.25. Moreover, Valero’s PEG ratio is exceptionally low at 0.56, and the Enterprise Value/EBITDA ratio is also extremely low at 4.19, the sixth lowest among all S&P 500 stocks. According to James P. O’Shaughnessy, the Enterprise Value/EBITDA ratio is the best-performing single value factor. In his impressive book “What Works on Wall Street,” Mr. O’Shaughnessy demonstrates that 46 years back testing, from 1963 to 2009, have shown that companies with the lowest EV/EBITDA ratio have given the best return.

In addition, Valero is committed to disciplined capital allocation and to returning cash to stockholders. The company said that its goal in 2015 is to exceed 2014’s total payout ratio. In 2014, Valero returned $1.9 billion to stockholders, or 50% of net income from continuing operations, with $554 million in dividends and $1.3 billion in stock buybacks. In January 2015, Valero announced a 45% increase in its quarterly common stock dividend from $0.275 per share to $0.40 per share. The forward annual dividend yield is at 2.78% and the payout ratio only 16.6%. The annual rate of dividend growth over the past three years was very high at 51.8%, over the past five years was at 11.8%, and over the past 10 years was very high at 21.9%.

Raad why Ari likes it: Why Valero Energy Stock Is A Great Buy Right Now – Valero Energy Corporation (NYSE:VLO) | Seeking Alpha

For all the latest news and podcasts, join our free newsletter here.

Don’t forget to check out our FREE Large Cap 1000 – Stock Screener, here at The Acquirer’s Multiple: