As part of a new series, each week we typically conduct a DCF on one of the companies in our screens. This week we thought we’d take a look at one of the stocks that is currently in our screens, The Home Depot Inc (HD).

Profile

Home Depot is the world’s largest home improvement specialty retailer, operating more than 2,300 warehouse-format stores offering more than 30,000 products in store and 1 million products online in the US, Canada, and Mexico. Its stores offer numerous building materials, home improvement products, lawn and garden products, and decor products and provide various services, including home improvement installation services and tool and equipment rentals. The acquisition of Interline Brands in 2015 allowed Home Depot to enter the MRO business, which has been expanded through the tie-up with HD Supply (2020). The additions of the Company Store brought textiles to the lineup, and Redi Carpet added multifamily flooring, while the recent tie-up with SRS will help grow professional demand.

Recent Performance

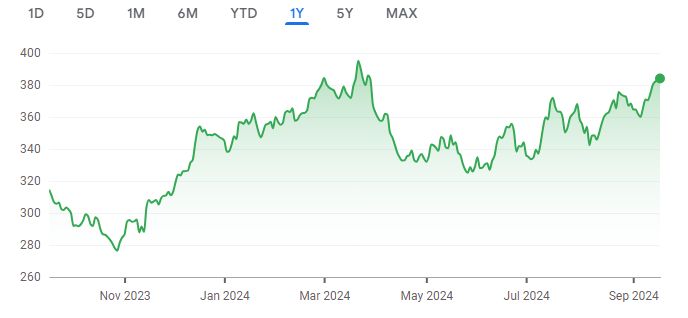

Over the past twelve months the share price is up 22.06%.

Source: Google Finance

Inputs

- Discount Rate: 7%

- Terminal Growth Rate: 3%

- WACC: 7%

Forecasted Free Cash Flows (FCFs)

| Year | FCF (billions) | PV(billions) |

| 2024 | 16.86 | 15.68 |

| 2025 | 18.36 | 15.89 |

| 2026 | 19.98 | 16.08 |

| 2027 | 21.75 | 16.29 |

| 2028 | 23.67 | 16.49 |

Terminal Value

Terminal Value = FCF * (1 + g) / (r – g) = 541.78 billion

Present Value of Terminal Value

PV of Terminal Value = Terminal Value / (1 + WACC)^5 = 377.38 billion

Present Value of Free Cash Flows

Present Value of FCFs = ∑ (FCF / (1 + r)^n) = 80.43 billion

Enterprise Value

Enterprise Value = Present Value of FCFs + Present Value of Terminal Value = 457.81 billion

Net Debt

Net Debt = Total Debt – Total Cash = 48.48 billion

Equity Value

Equity Value = Enterprise Value – Net Debt = 409.33 billion

Per-Share DCF Value

Per-Share DCF Value = Enterprise Value / Number of Shares Outstanding = $412.22

Conclusion

| DCF Value | Current Price | Margin of Safety |

|---|---|---|

| $412.22 | $384.01 | 6.84% |

Based on the DCF valuation, the stock is undervalued. The DCF value of $412.22 share is higher than the current market price of $384.01. The Margin of Safety is 6.84%.

For all the latest news and podcasts, join our free newsletter here.

Don’t forget to check out our FREE Large Cap 1000 – Stock Screener, here at The Acquirer’s Multiple: