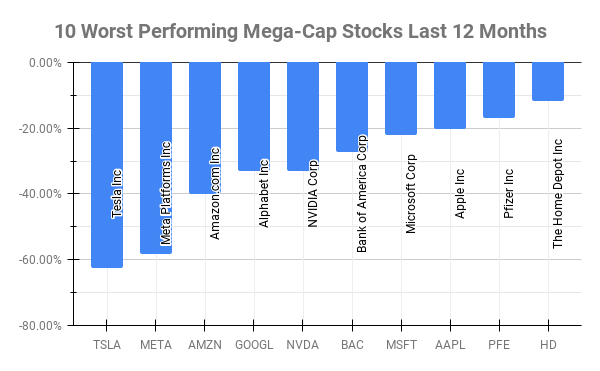

Over the past twelve months ten Mega-Cap stocks have underperformed all others. Mega-Caps are defined by $200 Billion Market Cap or more. Here’s this week’s top 10 worst performing Mega-Caps in the last twelve months: Symbol Name 1 Year Price Returns (Daily) TSLA Tesla Inc -62.51% META Meta Platforms Inc … Read More

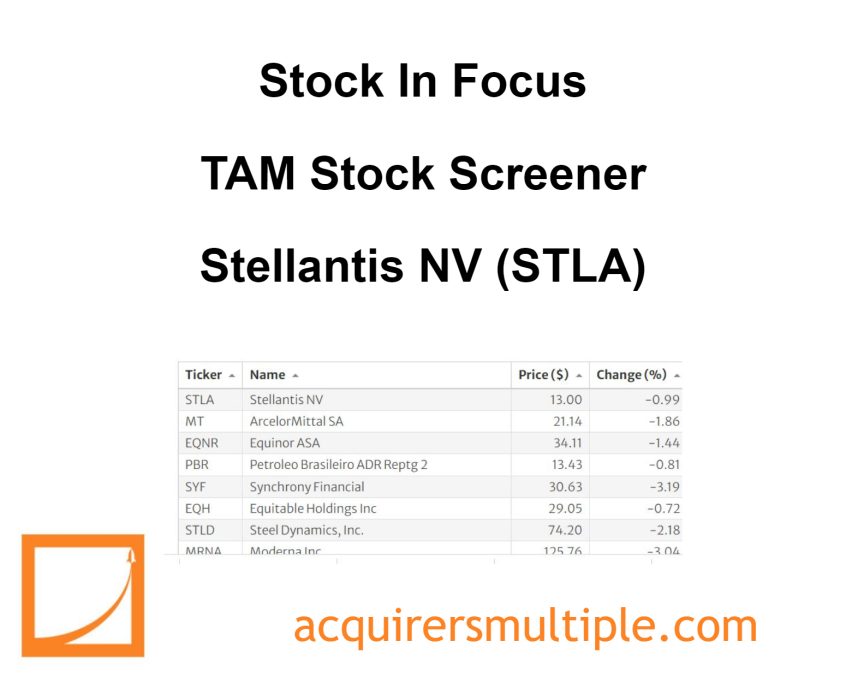

Stock In Focus – TAM Stock Screener – Stellantis NV (STLA)

As part of our ongoing series here at The Acquirer’s Multiple, we provide this feature article titled ‘Stock in Focus‘ where we focus on one of the stocks from our Stock Screeners. One of the cheapest stocks in our Stock Screeners is: Stellantis NV (STLA) Stellantis NV was formed on Jan. 16, 2021, … Read More

This Week’s Best Value Investing News, Podcasts, Interviews (1/20/2023)

This week’s best investing news: David Einhorn – Greenlight Capital Q4 2022 Letter (GC) Regulating Crypto – Democratization and “The Bucket Shop Problem” (Jamie Catherwood) Oaktree’s Howard Marks on Markets, Fed Rates, Inflation (Bloomberg) Inside the High-Yield Spread (Verdad) What if Tesla Is…Just a Car Company? (WSJ) Mastering the Mental … Read More

Bill Miller Shorts Tesla

In their latest episode of the VALUE: After Hours Podcast, Brewster, Taylor, and Carlisle discuss Bill Miller Shorts Tesla Here’s an excerpt from the episode: Tobias: Samson says that Bill Miller has a short on Tesla. That’s very un-Bill Miller like, isn’t it? Bill: Oh, I heard Bill Miller’s portfolio is really … Read More

This Acquirers Multiple Stock Appearing In Dalio, Simons, Cohen Portfolios

Part of the weekly research here at The Acquirer’s Multiple features some of the top picks from our Stock Screeners and some top investors who are holding these same picks in their portfolios. Investors such as Warren Buffett, Joel Greenblatt, Carl Icahn, Jim Simons, Prem Watsa, Jeremy Grantham, Seth Klarman, Ray Dalio, … Read More

David Einhorn: We Benefited By Shorting ‘Innovation’ Stocks

In his recent Q4 2022 Letter, David Einhorn explained how he benefited by shorting so called ‘innovation’ stocks. Here’s an excerpt from the letter: We are nothing if not persistent. In March of 2021, we again believed that the bubble had popped… this time correctly. We created our third bubble … Read More

Howard Marks: Forget Good Idea/Bad Idea, Think Risk/Return

During his recent interview with Bloomberg, Howard Marks explains why investors should think in terms of risk/reward and not good idea/bad idea. Here’s an excerpt from the interview: Marks: After Milken and others arrived in 77-78, the new way of thinking was well it’s not a great company but the … Read More

ARKK Flat For Past 5 Years

In their latest episode of the VALUE: After Hours Podcast, Brewster, Taylor, and Carlisle discuss ARKK Flat For Past 5 Years. Here’s an excerpt from the episode: Tobias: This is another thing we were talking about before we came on, but do you think that the flows to something like … Read More

One Stock Superinvestors Are Selling

As part of the weekly research here at The Acquirer’s Multiple we’re always interested in superinvestors who hold the same stocks that appear in our Acquirer’s Multiple Stock Screeners, based on their latest 13F’s. Investors such as Warren Buffett, Joel Greenblatt, Carl Icahn, Jim Simons, Prem Watsa, Jeremy Grantham, Seth … Read More

Pzena: The Value Opportunity Is Compelling

In their latest Q4 2022 Letter, Pzena Investment Management explain why the value opportunity is compelling. Here’s an excerpt from the letter: Despite recession, inflation, and geopolitical fears, we believe the value opportunity is compelling, even after its best relative performance in more than two decades. Macroeconomic and geopolitical fears … Read More

David Einhorn: A ‘Debilitated’ Value Investing Industry Is Great News For Us

In his recent Q4 2022 Letter, David Einhorn explained why a ‘debilitated’ value investing industry is great news for his firm. Here’s an excerpt from the letter: 2022 was an exceptionally good year. In many ways it was our best ever and is most comparable to 2001, the year after … Read More

Warren Buffett: You Don’t Have To Make It Back The Way You Lost it

In their latest episode of the VALUE: After Hours Podcast, Brewster, Taylor, and Carlisle discuss Warren Buffett: You Don’t Have To Make It Back The Way You Lost it. Here’s an excerpt from the episode: Jake: Yeah. I don’t know the answer. I’ve wondered if it would be a useful model … Read More

One Stock Superinvestors Are Buying

As part of the weekly research here at The Acquirer’s Multiple we’re always interested in investing gurus who hold the same stocks that appear in our Acquirer’s Multiple Stock Screeners, based on their latest 13F’s. Investors such as Warren Buffett, Joel Greenblatt, Carl Icahn, Jim Simons, Prem Watsa, Jeremy Grantham, … Read More

Warren Buffett: The Stock Market Is The Most Obliging, Money-Making Place In The World

During the 2012 Berkshire Hathaway Annual Meeting, Warren Buffett explained why the stock market is the most obliging, money-making place in the world. Here’s an excerpt from the meeting: WARREN BUFFETT: Yeah. We’ve run Berkshire now for 47 years. There have been several times — oh, four or five times … Read More

Aswath Damodaran: Stick To Your Philosophy Or Just Buy The Index

During this interview with The Millennial Investing Podcast, Aswath Damodaran discussed sticking to your philosophy of just buying the index. Here’s an excerpt from the interview: Damodaran: So to me sometimes companies make my list because I like to own them but I don’t like the price they’re at, but … Read More

Our 2023 Predictions

In their latest episode of the VALUE: After Hours Podcast, Brewster, Taylor, and Carlisle discuss Our 2023 Predictions. Here’s an excerpt from the episode: Jake: Okay. So, with that out of the way, happy birthday, Charlie. This is inspired by Jason Zweig, had a recent writeup that he called his Hindsight … Read More

Leon Cooperman: Learning From Henry Singleton

In this interview with Forbes, Leon Cooperman discusses what he learned for Henry Singleton. Here’s an excerpt from the interview: Cooperman: I learned a lot from studying Henry Singleton. He graduated number one in his class at the Naval Academy and got a Ph.D. in electrical engineering at MIT. He … Read More

Cliff Asness: If You Think You’re Right, HODL!

In this interview with Infinite Loops, Cliff Asness explains why if you think you’re right about an investment, you should hold on for dear life (HODL). Here’s an excerpt from the interview: Asness: It does not make all sock companies attractive at any valuation in any financial condition. I don’t … Read More

Charles Munger – Top 10 Holdings – Latest 13F

One of the best resources for investors are the publicly available 13F-HR documents that each fund is required to submit to the SEC. These documents allow investors to track their favorite superinvestors, their fund’s current holdings, plus their new buys and sold out positions. We spend a lot of time … Read More

VALUE: After Hours (S05 E1): 2023 Predictions, Market Crashes, Small Value, Don’t Make Predictions

In their latest episode of the VALUE: After Hours Podcast, Bill Brewster, Jake Taylor, and Tobias Carlisle discuss: Our 2023 Predictions Warren Buffett: You Don’t Have To Make It Back The Way You Lost it ARKK Flat For Past 5 Years What Is The Economic Case For Self-Driving Cars? Bill … Read More