Summary

In this episode of The Acquirer’s Podcast Tobias chats with Adrian Saville, who is the CEO and founder of Cannon Asset Managers in South Africa. Since the mid-1990’s Adrian has been running portfolios full of unloved but good businesses which have returned an average of 19.8%. During the interview he provided some great insights into:

– What Are The Four Attributes Necessary To Create A Successful ‘SuperDogs’ Portfolio

– What Is Unique About Investing In The South African Stock Market

– The One Reason Mean Reversion Is So Powerful – This Too Shall Pass!

– Investors Can Find Some Of The Best Opportunities In The Smallest Listed Companies

– The Comparisons Between Sabvest and Berkshire Hathaway

– How Does One Company Make Up 20% Of The South African Stock Market

– What Are The Benefits Of Running An Investment Firm And Teaching University Students

Also, here is the marketing collateral mentioned in the interview – Cannon-Asset-Managers-Acquirers-Multiple-2019Q2.

The Acquirers Podcast

You can find out more about Tobias’ podcast here – The Acquirers Podcast. You can also listen to the podcast on your favorite podcast platforms here:

Full Transcript

Tobias Carlisle: Okay, you ready?

Adrian Saville: I’m good.

Tobias Carlisle: Let’s do it. Hi, I’m Tobias Carlisle, this is The Acquirers podcast. My special guest today is Doctor Adrian Saville, he’s the CEO and founder of Cannon Asset Managers in South Africa. He’s also a professor of economics at the University of Pretoria. He’s got some fascinating ideas, and I’m looking forward to having a chat with him right after this.

Speaker 3: Tobias Carlisle is the founder and principal of Acquirers Funds. For regulatory reasons he will not discuss any of the Acquirers Funds on this podcast. All opinions expressed by podcast participants are solely their own and do not reflect the opinions of Acquirers Funds or affiliates. For more information visit acquirersfunds.com

Tobias Carlisle: Hi Adrian, how are you?

Adrian Saville: I’m good Tobias, thanks for inviting me onto the podcast and the time with you.

Tobias Carlisle: My absolute pleasure. I should say in the intro, full disclosure that we recorded a podcast yesterday and I lost the file so this is not the podcast, this is a tribute to the podcast. But, we’re going to do our best to recreate the magic that we had yesterday.

Adrian Saville: Second time better.

Tobias Carlisle: Tell us a little bit about your Superdogs portfolio.

Adrian Saville: Superdogs started really as a, I guess an academic curiosity where in the mid 1990s I wondered what would happen if I built a portfolio of unloved but good businesses. I think it’s academically honest to describe it exactly as that. It wasn’t that I had some spectacular foresight, or strong inkling of what I would get. I really did just wonder what would happen if I put together this portfolio.

Adrian Saville: I constructed in, for the first time 1996, a highly diversified portfolio made up of financial and industrial companies listed on the Johannesburg stock exchange with really just two criteria for inclusion. The first was that the business had to be profitable, and the second was that it had to be unloved, and drawing them from a wide range of industries, all the way from engineering and electronics through to banking and insurance. I constructed that first portfolio and it happened to have a spectacular year, and the curiosity turned into intrigue.

Tobias Carlisle: How big was the first year?

Adrian Saville: First year was a 34% return, which I guess in any environment is notable. It was against a market return of just 2.5%, so I’m not sure if we’re allowed to use the word alpha in this conversation [crosstalk 00:03:20]

Tobias Carlisle: You can use it, there’s a lot of alpha there.

Adrian Saville: But, relative to market, it was just an absolutely extraordinary result. Our industry scratches around for a few basis points or modest percentages, and to have banked that in the first year led me to repeat the exercise in year two, was followed by a second year of really healthy returns, 21% in the second year, and that has been the practice from them. Superdogs is now a 24 year old portfolio.

Tobias Carlisle: And, you’ve averaged about 19.8% versus 13.9% for the broader index, which is almost four points of out performance, which is extraordinary over a very extended period of time. Can you just tell us a little bit about how you’re defining unloved, or how you were defining unloved initially?

Adrian Saville: Well, initially it was that the business had to be profitable, which would I guess infer, or could be inferred that it was unfairly unloved, or perhaps it could at least justify a tiny bit of love. But, the unlovedness was captured by a single metric, price earnings multiple. With the benefit of hindsight, that single metric is narrow and naïve, and having been a very keen follower and enthusiastic reader of your work, I don’t have to tell you that we could easily have refined that to a far more sophisticated metric, but that’s where we started. It needed to have positive earnings, low price relative to those earnings and we were away.

Adrian Saville: Over the years we’ve added components to that. Very early on we added dividend yield, which required then that the earnings were underpinned by distribution. We then added price book, which suggested that there was a balance sheet behind the earnings, and global financial crisis in particular implored us to add a quality component.

Tobias Carlisle: And, what’s your quality component? How are you defining quality?

Adrian Saville: Range of factors go into quality. We start with a forensic tool, which I think is relatively unique to the industry. In version one of our podcast we didn’t speak about this, so it’s great to be sharing some new content with you. But, we start with a forensic tool, which really goes on the recognition that if it’s garbage in you’re going to get garbage out, and if there is accounting error, or accounting fraud in any business analysis you really are just working with a fiction.

Adrian Saville: So, over the last 20 years or so we’ve built a, I think, a fairly sophisticated and quite powerful tool that helps us identify the quality of numbers, and once we’re satisfied that we’re working with robust figures we then start to move into strength of balance, quality of operating performance, stability of operating performance, never confusing accounting profit with cashflow profit. The first is a result of a whole bunch of rules, the second is a result of business performance. So, we’re not after accounting earnings, we’re after cashflow earnings, and the way in which we, sort of at a headline level measure business performance is through tools like Joseph Piotroski’s F-Score, would be an example.

Tobias Carlisle: And, you’ve refined that over the years. I actually don’t mind price to earnings as a metric. I think it’s underrated, because one of the things it looks for, you have to be profitable in the first instance for it to have a price to earnings ratio, and then it’s a flow. I think it’s a pretty good metric, but naturally you have to add quite a lot more onto it. I’ve read that you have, in some of the collateral that you sent to me, you have four key elements as part of your process, could you just discuss those briefly?

Adrian Saville: Sure, so the first attribute is to look for value in an entity. Value can be measured in a range of ways, price earnings is a point of departure and that was our very first jump off point now almost 25 years ago. You can add to that dividend yield, price book, price cashflow, so we work with a range of metrics and tools, and measures to identify the inherent or intrinsic value in a business. Not valuing it, or valuation, just to ask from what you see what you get is their worth in the enterprise.

Adrian Saville: We happen to include in that a [Ben Graham 00:08:28] tool, which over the years has flagged for us a useful number of Ben Graham net-net’s. We’ve recently invested in one of those in the insurance sector, and by absolute coincidence about ten years ago we found an extremely profitable, fantastically priced Ben Graham net-net that went on to be a classic ten bagger for us, a company called Conduit Capital.

Adrian Saville: The second attribute is to look for the quality of the business, referencing the earlier point that we want to buy good businesses. Ideally, we want to buy great businesses, but to borrow in some part from your work we are very comfortable buying good businesses at great prices. Ideally, we’d like to buy great businesses at great prices, but very happy buying good businesses at great prices. Quality can be measured in a range of ways Piotroski F-Score is a headline measure. Cash conversion, so that earnings convert to cashflow, that we’ve got ideally stable margins, stable ROE’s, stable ROA, relative to, always relative to. You can’t analyze or assess a business in its own right.

Adrian Saville: And then, the third attribute from there is to work out what the entity, what the enterprise is worth, and here too we have a range of approaches to think about a business valuation, and step four is to, from those three pillars, construct a portfolio with a range of elements including diversification, or concentration that is suited to the mandate that we’re building too.

Adrian Saville: One of my favorite portfolios is called Hummingbird, it holds just ten names. We built a global equity portfolio that holds just 25 names, it’s benchmarked against MSCI all world index, but it’s not trying to mimic the index, it’s trying to beat the index by a healthy margin, and we’re very comfortable holding a small number of names up against a very diversified global index. Superdogs tends to hold 40 or 50 names.

Adrian Saville: Once we’ve constructed the portfolio, I think a part of the process that very often falls into neglect is the sell process, is managing and monitoring, and maintaining the positions, that when something is no longer investible we have the discipline to remove it from the portfolio, and we don’t land up with long tails, or overly diversified portfolios.

Tobias Carlisle: So, your focus is value for the most part, but you offer some different portfolios through the firm, could you just take us through your offering?

Adrian Saville: Sure, the portfolios sit on a spectrum that ranges from active to passive, and from domestic to global, so you can think of your classic business school, two by two, and in the passive we’re building, generally, multi-asset portfolios. Those multi-asset portfolios have two imperatives, the one is to mimic or match the asset class that we want to own, and the second is to make sure that costs are out of the system.

Adrian Saville: On the active side of the portfolio spectrum as names like our Hummingbird will suggest we’re quite comfortable looking very different to market. It’s more expensive to run, it has a high element of intellectual property in it, and so we’ll range in our portfolio construction from passive, market matching, or asset class matching, multi-asset all the way through to highly concentrated, high conviction active. We generally don’t hang around in the middle where we see the industry tending to crowd, and trying to beat each other in what is very often a one-legged person in … I think Charlie Munger put it, a one-legged person in an ass kicking contest. So, we push to either side of the spectrum. Passive, multi-asset, very low cost, or active, high concentration, high conviction.

Adrian Saville: And then in terms of growth or capital protection here, a far more graduated, or phased approach where we will range all the way from robust, capital protection or preservation, through to income generational yield, and then at the top of that pyramid, capital growth.

Tobias Carlisle: Your passive market index style, it’s not market capitalization? You offer, is it [inaudible 00:13:52], or you do offer that as well?

Adrian Saville: Sometimes we’re obliged to invest in or hold what’s available, especially if it’s a modest component of a multi-asset portfolio. An example would be if we were putting in a global biotech tracker. We might take then what’s available and it will be off the shelf. I don’t mean that in an insulting way in any shape or form. There is a fantastic range of solutions available, but where we have the capacity to add investment, intelligence or wisdom we will try and reshape some of those passive solutions.

Adrian Saville: One of my favorite examples is in the South African equity arena, where overwhelmingly the South African equity market is characterized by concentration, so a handful of stocks make up 50% of the index, and then a very, very long tail. And, our preference is to replace then, that skewed, and often poorly behaved market weighted index with an equal weighted index. As long as you’ve got a long enough runway, and you’re not obsessed by the month-to-month or quarter-to-quarter market return, as functional or dysfunctional as you might regard it, that equal weighted portfolio tends to produce much better risk adjusted returns, or what I prefer to refer to as results, just much better investment results than your market weighted index.

Tobias Carlisle: Value has struggled globally for about the last decade, and in particular for the last five years. What’s the South African experience been?

Adrian Saville: Well, you commented initially on some of the collateral I’ve shared with you, and so you’ve got a good sense of how our Superdogs and Hummingbird portfolios have done in recent times. The last five years, perhaps even the last ten years in sympathy with global value factors have been tough yards. Global financial crisis, we navigated that in reasonable form and then it was a rather spectacular recovery from global financial crisis. From then to now though, and what I’m referring to is 2009-2010 to roughly now, the value environment in South Africa has been, it’s been hard going, tough yards.

Adrian Saville: I think there’s a couple of elements that explain that, the one is as you point out, the rather anemic global appetite for value, where it’s been very much a growth on unicorn, low-cost of capital environment. That has been … To add the insult to the injury, South Africa has had, on top of that, a tough domestic economic circumstance, and you’ll appreciate value mathematically tends to be small and out of favor, and it happens to be because of the uniqueness’ or specific elements going on in South Africa over the last ten years. It is South African facing businesses that have fallen into value territory, and put in a short statement, the appetite just hasn’t been there.

Adrian Saville: So, you’ve had lack of global appetite, compounded by an even lower domestic appetite for value. The net result is, when we construct our Superdogs portfolio at the beginning of this year, we’re constructing portfolio on a seven times earnings multiple.

Tobias Carlisle: And, what’s the broader market at?

Adrian Saville: 15 times.

Tobias Carlisle: So, it’s less than half price relative to the market.

Adrian Saville: We’re trying to pay the classic 50 cents on the dollar, that’s exactly what we’re looking for. So, if we are buying a portfolio of good businesses, dividend paying, strong balance sheets, and we’re paying half the earnings multiple, and they have the ability to earnings revert to recapture performance then we have paid 50 cents on the dollar, and that’s what our 20 year track record suggests, or evidences.

Tobias Carlisle: The markets that I’m most familiar with are the Australian market has that unusual composition where it’s about 50% financials and about 15% basic materials, quite similar to the Canadian market. How is the South African Market composed?

Adrian Saville: South Africa, although the economy is, I think regarded and driven by commodity and resource components, the Johannesburg stock exchange itself has actually a relatively modest representation of commodity businesses. They make up at the moment, about 20% of the Johannesburg stock exchange. The balancing 80% is made up of financials, 20-30%, and then industrials is the bulk, the heft, 50% of the market. There are times when commodities have come to make up a much larger component. At the peak of the resources boom in the noughties decade, commodities made up about half of JSE market cap.

Tobias Carlisle: And, the South African market is a little bit unusual at the moment in that it’s got one stock that’s very heavily weighted, and I think it’s a great story too, and I’m going to mispronounce it, but Naspers, Naspers [crosstalk 00:19:49]

Adrian Saville: No, you got the pronunciation absolutely [crosstalk 00:19:49]

Tobias Carlisle: Can you just tell us a little bit about the Naspers?

Adrian Saville: Sure, to take a step back just before we just into Naspers, you’ll appreciate being familiar with Canada, Australia, and the vagaries of commodity cycles, that in itself makes it tough if you set out to beat the market, and you’ve got one component, that can be 20% or 50% depending on the mood. That part is bouncing around, and then to add complexity to that already reasonably demanding challenge you’ve got industrial concentration. That concentration takes the shape as you flag in the current environment with Naspers making up about 20% of the index.

Adrian Saville: That company has a long South African history, it’s more than 100 years old, and starts its life as a print media business, printing newspapers, that’s where its life starts. Over the years it has demonstrated a characteristic an innate attribute of being willing to adventure into neighboring industries. So, it’s got into book publishing as a case in point, as the South African education system grew. More recently, through the 1980s and into the 1990s it went into broadcast media, and in particular digital satellite television. The company that today is separately listed is called DSTV, very successful, profitable footprint, pan-African in market reach, and extending that attribute of being a willing venture capitalist, or adventure capitalist even, Naspers through the 1990s and into the noughties made some modest investments into Chinese eCommerce businesses.

Adrian Saville: One of those ventures led them to acquiring about half of the equity of Tencent, which today is one of the largest eCommerce businesses globally, not just China. Naspers has a substantial economic stake in that business. It has translated into Naspers being … Well, A, 20% of the Johannesburg stock exchange, but that aside, in and of itself, a spectacularly successful investment for anyone who has been willing and patient to own it for a long time.

Tobias Carlisle: And, what proportion of Naspers value is attributable to Tencent?

Adrian Saville: You’ll love this Toby, more than 100%.

Tobias Carlisle: So-

Adrian Saville: You’ve got [crosstalk 00:22:59] [inaudible 00:23:00].

Tobias Carlisle: I’ve seen the writeup quite a few times over the last two or three years at least where you have an arbitrage where you can arbitrage Tencent out of Naspers, because Naspers has some other good assets in it. But, I think it’s a fascinating story. It’s funny how the impact of it has been so huge through the company itself and through the index.

Adrian Saville: Yeah, so Naspers as you point out, owns underlying assets. I mentioned DSTV as a case in point, it has a healthy pile of cash. I think that much doesn’t need explanation, and it’s made investments into other businesses, including Mail.ru, Facebook. It has small stakes in those, and those are interesting. It doesn’t characterize Naspers as a unicorn investor, it just happens to be that over the way it’s gathered up those positions, and if you are paying 100 rand for a Naspers share, you’re getting about 130 rand in net asset value. The bulk of that net asset value being explained by Tencent, so there’s a fantastic arbitrage.

Adrian Saville: South Africa has a very sophisticated financial sector, well established, competitive and sophisticated, and unsurprisingly then that financial sector has given birth to Naspers residuals. You can buy a stub or the rump of Naspers, which gives you exposure to whichever component you want. So, lots of ways to be exposed and invested in the core business, as well as its satellites.

Tobias Carlisle: It must make it very difficult to construct a portfolio, because you have to keep your eye on Naspers all the time because it’s such a huge component of the index, and you have to make an active decision one way or the other. If you hold it, that’s an active decision to be long even in a passive index. Or, you have to construct something that … How do you deal with that?

Adrian Saville: Not to be flippant, but one way that you can deal with it is to make a strong argument for an equal weighted index. There will come a time when Naspers is no longer 20% of the market. It’s hard to know what the factors will be that cause that to happen, but in our philosophy we place very little weight or value on forecasting. So, whilst we don’t know what’s going to change Naspers from being a 20% factor to much smaller, we know that something will change. There was a time when Anglo American, and BHP Billiton made up 30% of the JSE, they now make up less than 10%. It was hard to forecast when the global financial crisis would strike, but that’s what changed it.

Adrian Saville: So, you can think about portfolio construction ways of dealing with this in terms of your broad rules, market weighted, equal weighted, or we don’t step more than X percentage points away, or basis points away from whatever the market weight might be to close down tracking errors. So, there’s lots of ways that you can cope with it. If you want to be ultra-active then you are either going to need to own more than 20% in your portfolio, or if you don’t like it and you want to be absolutely no dead capital, then you’ve got to take that beta position from 20 all the way down to 0. You’re going to be spectacularly right or spectacularly wrong. It really does make for a challenging portfolio construction environment, and it has led to fierce and furious debate in our investment team over many, many years, we have not yet solved it.

Tobias Carlisle: So if you would, let’s go through some of your positions. We discussed several of these yesterday, but I noted them in your collateral as well. Sabvest, I think was the … I hope I’m pronouncing that correctly.

Adrian Saville: Yeah. Sabvest is, I think it’s a neat company to talk about because I have already alluded to South Africa being a well regulated and relatively sophisticated market. Very often, when people look at mid and smaller sizes businesses their risk radar immediately goes up. But, if you have a well regulated market then a large part of systemic risk, I think is catered for. That gives us great comfort in exercising what I believe is one of Cannon Asset Managers strong competitive strengths, and that is the ability to move out of the highly traded, larger part of the market.

Adrian Saville: So, South Africa has almost sort of a two-legged market. The first leg is your top 100 companies or so. They tend to be well traded, very liquid, highly researched, and researched not just domestically but globally. Once you’ve moved outside of that top 100 you’re still in companies that have a healthy size and good liquidity, but the coverage and the extent of research on these businesses, it’s as if you step of a roadrunner research cliff and nothing happens at stock 101. You’re then left with 3 or 400 stocks, which are in each of their rights, an investment option, but massive information gaps.

Adrian Saville: I think that’s where just a tiny bit of research and information gathering can actually lead to quite pronounced information advantages, and Sabvest, to get to your question is a great case in point. The company is started by Christopher Seabrooke, and he listed Sabvest on the Johannesburg stock exchange in the late 1980s. It started with a primary asset being a textiles, fittings and fasteners business, doing zippers and linings, and buttons and press studs. That company was part of, at the time, a very vibrant South African clothing and textiles industry.

Adrian Saville: Over the years that industry has wound down and two interesting things have happened in the Sabvest story. The first is, Chris Seabrooke has successfully migrated the footprint of SA buyers, which is the Sabvest clothing and textiles business, from being South African based to being South East Asian foot printed, so that’s been a successful international migration. The second is, over the year’s he’s steadily used the cashflow of that initial business to build a portfolio that is, I think successfully diversified, and the success of that diversification is evidenced by a return on equity over 20, where are we? 30 years of being a listed company. 30 years as a listed company. 22% return on equity, that’s an impressive result in anyone’s language.

Adrian Saville: To get to the point of when or why did we invest, a few years back … We followed the company for many years, and we have been invested and disinvested at different stages, but about three years ago you were able to acquire stock in Sabvest at 22 rand a share with an underlying net asset value in our estimate of about 50 rand a share. So, we were paying 40 or 50 cents in the rand for this fantastic asset, a large part of which was hard currency, dollar-based earnings, usefully diversified, or healthily diversified. Then, through the course of the last 12 months we weren’t sure what the catalyst would be in terms of releasing that capital trap. We had some suspicions, and one of those suspicions was a liquidity trap that didn’t matter how much you loved the stock, you just couldn’t trade it.

Adrian Saville: So, it took us a long time to build that position, but through the course of last year three things happened. The first was, they sold off their international textiles business, fittings and fasteners business, and that released cashflow onto the balance sheet. That was an impressive corporate event in terms of capital release. The second was a very long standing shareholder, one of the founding family businesses released their share block into the market and that has helped liquidity lift materially. The third was, they used the duality of those two events to buy back some of their own shares with that free cashflow, and that I think sent a really clear signal to the market. So, with those three events having taken place the 22 rand quickly turned into 50 rand, and we’ve been thrilled with the result over the last 12 months.

Tobias Carlisle: I think it’s worth pointing out that the gentleman’s name, the CEO of Sabvest … I’m sorry, I’ve just-

Adrian Saville: Christopher Seabrooke.

Tobias Carlisle: Christopher Seabrooke, he has returned 54 times on capital since 1988, and so the parallels are striking. He started with a textile business, and he’s transitioned out of that through investing and returned 54 times on capital. It sounds very reminiscent of Warren Buffett’s own story with Berkshire Hathaway.

Adrian Saville: It’s a wonderful parallel, and I don’t think it’s by design. It’s just fantastic coincidence. In our opinion, as longstanding share holders of the business, we regard Chris as one of the shrewdest allocators of capital in South Africa, and despite this extraordinary track record he remains, from an institutional perspective, largely uninvested, that institutions just don’t follow him because he’s outside of this top echelon.

Tobias Carlisle: That’s very Buffett like.

Adrian Saville: Yeah.

Tobias Carlisle: So, let’s talk about Telkom.

Adrian Saville: Well that’s a second stock that, and now to talk a little bit against myself, Telkom is inside of the top 100. Telkom is historically South Africa’s state owned telecommunications business. It’s an old landline business, copper cabling buried in the group. As mobile came into the industry, Telkom was one of two companies to get a mobile license, the other was a business called MTN, and over the years the two of them grew in parallel building up very successful mobile cellular businesses alongside Telkom’s landline copper business.

Adrian Saville: A while back, Telkom spun out that mobile business, it’s called Vodacom, and so that gave the South African market three listed telcos, MTN, Vodacom and Telkom. With Telkom overwhelmingly being regarded as the ugly sister in that trio. It was on the back foot, it was old, it’s infrastructure was buried in the ground. There was a lot of net asset value being done on the business to suggest that they had more copper in the ground than their market cap. It was one of their favorite throwaways about Telkom, and there too.

Adrian Saville: We have been invested for some time, but we were especially intrigued early last year where Telkom was trading at about 45 rand a share with a market cap of 30 billion rand. It was profitable, evidenced by a price earnings multiple of seven, a dividend yield of six, and very much a utility like return on asset and return on equity, so a return on asset of 10-11%, and a slightly better return on equity because there’s some modest gearing in the business, but for all intents and purposes what you would expect to see from a mature utilities business.

Adrian Saville: When we worked on trying to establish the value of that free cashflow as an operating business, we got to a share price that was a long way north of the 45 rand. We figured it was worth 70 odd rand a share, just as an operating business, and that compelled us to take a position. What was even more compelling though, was in our assessment, in our research we identified an underlying asset, a property business called Gyro, and that Gyro owns masts and towers as well as Telkom’s client service centers and office buildings. As far as we could establish nowhere in Telkom’s valuation was there any recognition of that property asset, and to us that was notable because the insured value of that property asset was 24 billion rand, and Telkom’s market capital was 30 billion rand. You can do the accounting gymnastics here in a range of way, but we thought one way of thinking of this is, we’re going to pay 6 billion rand for this operating asset. That could be one way of looking at it [crosstalk 00:38:34]

Tobias Carlisle: That you figured was worth 70 billion rand.

Adrian Saville: Which we thought was … Yeah, and we don’t have any insight here. We don’t have any fast track or any privileged information, but our suspicion is that much like Vodacom was spun out, that Gyro will be spun out of that holding company, and that that would release, in our estimate anywhere between 20-30 rand a share, and we were paying just north of 40 rand for the company. So, put it all together, 45 rand for the telco, mature, not fast growing, but strong cash flows, dividend paying. We thought that 45 rand was worth 75 or 80 rand and then add another 20 or 30 rand for the property business. We saw fantastic upside in it. Thankfully that hypothesis, that thesis has come to play, and Telkom today is trading on the market at 90 rand a share having just two days ago released very impressive results.

Tobias Carlisle: How do you size something like that in your portfolios?

Adrian Saville: With the benefit of hindsight, as big as possible, never enough.

Tobias Carlisle: Isn’t that the truth?

Adrian Saville: It really does depend on the mandate that we are building to, so if this is Hummingbird, I’ve said that name often enough that I guess people tuned in will know that this is one of my favorite portfolios. We’re quite comfortable owning 10% of the portfolio in a single name. If it’s a portfolio where the mandate is grow the capital, don’t take out sized risk, then we’re going to be holding a 20 or perhaps 30 stock portfolio, and our position is going to be a 3, maybe a 4% position. In those diversified portfolios where the guidance is initially prudence and you might be looking after retirement assets, or pension fund assets then you have to worry first about capital protection before you worry about capital growth. So, we’re going to be far more prudent in the size that we take in a company like Telkom. But, what we won’t own is, we own .5%. We just don’t see the merit in that. You can’t own .5% and charge active fees.

Tobias Carlisle: So, is Superdogs a little bit more systematic, and Hummingbird is a little bit more discretionary, and you do a little bit more work on Hummingbird than you do on a Superdog position?

Adrian Saville: I think that’s a fair descriptor. Superdogs is mechanically rebuilt every year. Early January we screen the entire market. We exclude resource companies from that screening because of their innate cyclicality, Superdogs then has a universe of financial and industrial companies. The businesses must have been listed for at least three years, that we’ve got sufficient data, they must be profitable, and then we go in search of the metrics that we spoke about earlier. From that, we will build a, for a sake of a number let’s call it a 40 stock portfolio. By convention, we hold three stocks per sector, and the sector is engineering, building, broadcast, insurance, banking. So, we will own three stocks per sector, and that gives us then this very diversified portfolio.

Adrian Saville: Over the years, over the 20 odd years of building Superdogs it became perhaps beyond coincidence that there were names that just kept being shown to us in the construction of that portfolio, and that, I think if you have a investment curiosity you’re going to roll up your sleeves and go digging, and that has led us to a number of really interesting businesses. When we last spoke I mentioned a company Indequity to you, our most recent Ben Graham net-net, and where we find those businesses, Superdogs, if it’s a 40 stock portfolio, you’re going to have 2% of the portfolio exposed to it. Hummingbird wants ten, and we will roll up our sleeves, we’ll engage with management, we’ll do deep due diligence on the business.

Adrian Saville: Not to speak lightly of our Superdogs, or other processes where the diligence is robust, but if you’re building a ten stock portfolio you have to do just that much more. The way that we speak about this amongst ourselves is, we regard Hummingbird as listed private equity that we want to invest in this business as if we owned the entire business for a very, very long time. So, Hummingbird is far more active, far more intimate, and our holding periods are much, much longer. Hummingbird is still a young portfolio, it’s been around for six years now and in that time we’ve turned over 15% of the portfolio. So, we’re very comfortable buying these stocks, and owning them as if we’re going to own them forever.

Tobias Carlisle: So, tell us a little bit about Indequity, because that was one that was, it was a fascinating discussion yesterday, so it’s a genuine nano cap and we should point out that the rand is, there’s about 15 rand to the dollar.

Adrian Saville: Correct.

Tobias Carlisle: But, I do love this story, and I love the fact that you know it so well even though you’re CEO Cannon, and you’re all over this tiny nano cap.

Adrian Saville: Yeah, we own a reasonable stake in this business now. We have been invested for a long time. Indequity, when we most recently increased our investment in the business, had a market cap of just over 30 million rand, that makes it tiny. [crosstalk 00:45:14]

Tobias Carlisle: It’s 2 million US.

Adrian Saville: In dollar terms, 2 million dollar. You corrected me yesterday when I said no one listening to this is going to be interested, and you said, “I don’t know.”

Tobias Carlisle: I don’t know, [inaudible 00:45:27] listen to this. This is what you get for staying to the end of the podcast. You [inaudible 00:45:33] nano cap that’s genuinely undervalued.

Adrian Saville: So, Indequity has … When we raised our stake recently, market cap of just over 30 million rand. On the balance sheet, 40 million rand in cash, no debt, and then along with the 40 million rand in cash a 1.2 million US dollar listed equity portfolio, so that 1.2 million US dollar is another 15 or 16 million rand. Add the cash and the listed portfolio together and you’ve got 55 million rand in highly liquid daily priced assets, cash and listed equity. The market cap is just north of 30 million rand, no debt on the balance sheet. In addition, the company is profitable, its most recent earnings 13 million. So, you’re paying 30 million for 13 million in earnings, that’s two or three multiple on earnings and dividend paying. That dividend translated into about a 10% dividend yield.

Adrian Saville: To add to all of this, our frustration is lack of liquidity, and the executive, the board is frustrating us further by acquiring and canceling their own shares. Immediately you go, “well, how am I ever going to realize value?” And, quite honestly if the investment horizon in Hummingbird is five, or ten, or forever then why do we want to realize the capital? We want this beautiful little business just to keep powering away, generating the earnings, and returning those earnings to us in the form of dividend, and another way in which you return earnings is you buy back and cancel shares. It’s not different to a very handsome dividend.

Tobias Carlisle: Much more tax efficient.

Adrian Saville: And much more tax efficient, so they’ve been buying back and canceling their own shares, which does leave you with a liquidity problem. We’ll live with that liquidity problem, and from where we made our most recent acquisition at about three rand a share, that share price has set up quite smartly, it’s now trading at around six rand a share, so the market cap has repriced. Even at these levels we think it is worth substantially more, just the insurance license carriers value, forget about the rest.

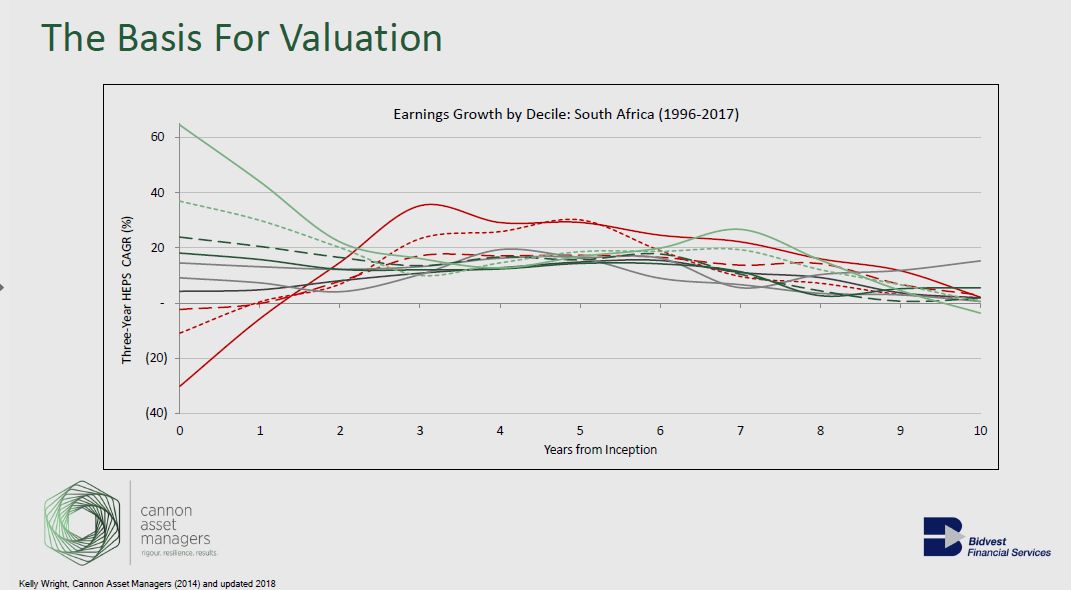

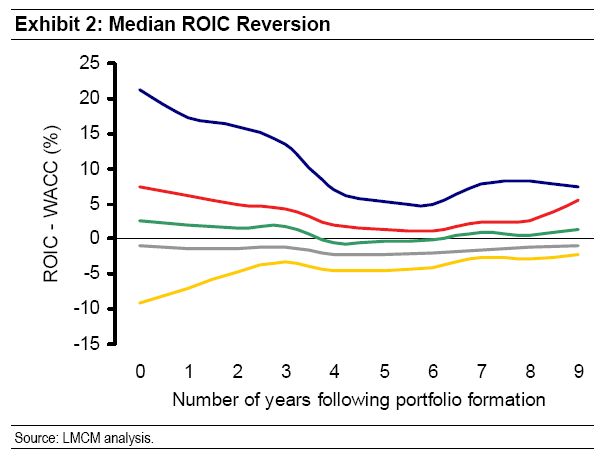

Tobias Carlisle: And, some of that marketing collateral you sent through to me, just to change gears slightly, you had a fascinating chart showing mean reversion in the return on invested capital of many of the companies in the South African stock market. So, let’s just describe that chart for us please.

Adrian Saville: The chart is one of the tools that we use to … Or, the evidence in that chart is one of the tools that we use to help us think about how to value a business. Most of the time businesses are valued as if they’re going to sustain their recent record, and if that recent record is disappointing then this is a business that’s in trouble, it’s going to enter the death zone, or if it’s a business that in the recent past has generated impressive results the industry habit is to straight line those in excel styled fashion. What the South African evidence points to is a very powerful force called mean reversion, and that businesses that have acceptable balance sheets, and viable models, if they are in a tough patch now the throwaway is this too shall pass, and how long does it take for this to pass? About three years, and mean reversion has kicked in.

Adrian Saville: By the same convention, businesses that have demonstrated impressive recent performance give up that record with the next three years or so. So, you have this convergence back to the mean, both in the laggards and the stars, both of them converting to the mean within a three or four year period, and if you push this further, five, six, seven years, once you’re out of five, six, seven years almost your entire universe is doing little more than returning a cost of capital. So, your return on invested capital for the market as a whole unsurprisingly is about your weighted cost of capital.

Tobias Carlisle: Yeah, I love that finding because I have that chart from Michael Mauboussin that I put up in a lot of my presentations, and a lot of my books that shows an identical…

Adrian Saville: Sorry, I’m interrupting you.

Tobias Carlisle: No, no please.

Adrian Saville: But it was his research that sparked us to do the exact same thing for South Africa, and well I wonder if that’s here, and absolutely, it’s here.

Tobias Carlisle: And perhaps even more so for some reason. It really stands out in that chart, that mean reversion is a real phenomenon.

Adrian Saville: Yeah, and I could give you in the current conversation, I could give you many names that in the last five or six years have gone from being absolute superstars a few years ago. If you ask the on the street investor what should you own they would’ve given you names like Mediclinic, and Medcare, and Mr. Price, and these businesses in the last two or three years, this mean reversion has really kicked in, and I hope I’m not saying that in a gleeful way. You don’t want bad things to happen to anyone’s investment or business, but it’s a really healthy reminder that stardom is hard to find, and even harder to retain.

Tobias Carlisle: You’re a professor of economics at the university of Pretoria, and this is no [inaudible 00:52:08] professorship, you’ve won multiple awards for teaching over a very long period of time. How do you juggle both, and what do you take from the academic side into your investing and vice versa?

Adrian Saville: [inaudible 00:52:23] I’m incredibly privileged to be able to do both of these things. I don’t think I’m unique. I can think of a number of other people in international markets who are able to look after two mandates. The simple reality is these two mandates feed each other in a very rich way, and what I’ll find in the business school classrooms, so my professorship is University of Pretoria, but it is part of the Gordon Institute of Business Science, which is a business school, and in any one year I will have 300-350 business school students who are in their 20s and 30s, and if you want a demanding, challenging audience who want to interrogate and due diligence your process there they are. So, it’s a fantastic environment to be challenged, to be kept up to date, to be reminded that we have never perfected this, that investing, it’s an ongoing learning process. It’s a safe environment in which you can share experiences, learn from successes as well as mistakes, and the two feed each other in a wonderful ebb and flow.

Tobias Carlisle: We’re coming up on our time Adrian, if folks want to get in contact with you, what’s the best way of doing that? I know you’re on Twitter, and so on.

Adrian Saville: Yeah, probably the easiest way, and I think in fact that’s how we initially engaged was on Twitter, it’s just to use my Twitter handle, it’s my name @Adriansaville. A-D-R-I-A-N S-A-V-I-L-L-E, otherwise you can find us on our business Twitter handle, which is @Cannonassets. Cannon is C-A-N-N-O-N, assets is plural, or pop me an email, Adrian@cannonassets.co.za, and if you find me through any one of those channels I’d love to engage.

Tobias Carlisle: And, I’ll make sure that all of that’s in the show notes to this show including the research that you’ve done, the marketing collateral that we were discussing earlier.

Adrian Saville: Thank you. Thank you.

Tobias Carlisle: Doctor Adrian Saville, it’s an absolute pleasure, thank you very much.

Adrian Saville: It’s great being with you, thank you for having me on your show, and I value the time with you.

Tobias Carlisle: My pleasure.

For all the latest news and podcasts, join our free newsletter here.

Don’t forget to check out our FREE Large Cap 1000 – Stock Screener, here at The Acquirer’s Multiple: