Is value a value trap?

Is the strategy itself destined to lose ground to the market while it gets cheaper, forever?

The theory of value is simple. Stock prices drift away from underlying values in the short term, and drift back towards underlying values in the long term. When the divergence between the price and the underlying value–Graham’s famous margin of safety–is wide enough, value investors bet on it closing. They anticipate mean reversion.

In practice, the drivers of returns to value tends to be lower multiples moving towards average multiples, despite depressed earnings tending to deteriorate. (Relative to glamour stocks, value stocks tend to have depressed earnings. Over the holding period the earnings tend to deteriorate further. See OSAM’s Factors from Scratch for more.) But here’s value’s one, simple trick: Multiple expansion tends to more than make up for the deterioration in the earnings.

The reason for the continued existence of the apparent margin of safety opportunity in value stocks is open to debate. The behavioral argument made by Lakonishok et al in Contrarian Investing (1994) relies on “naive extrapolation”–investors extrapolate trends in fundamentals and prices too far. Either those naive extrapolation investors ignore the propensity for mean reversion, or themselves create the conditions for mean reversion (or some combination of both). In their Cross-Section paper (1992) Fama and French make a “risk”-based argument that holds value stocks are riskier. The apparently higher returns are merely compensation for the added risk. I prefer the behavioral argument, but can’t rule out the risk argument. (The debate is a good example of Sayre’s Law. Another example can be found in the discussion over the merits of different valuation methods.)

TL:DR

- Value has underperformed for an extended time. Depending on how it is measured, that underperformance begins in 2005 or 2014.

- Value stocks are currently unusually cheap to their own averages. As long-only value has underperformed, the stocks in value portfolios have gotten more undervalued than usual, and the opportunity has gotten commensurately better.

- Historically, the presence of unusually cheap value stocks has preceded higher-than-average future returns for long-only value portfolios.

- Long/short value spreads are currently unusually wide. Over roughly the same time, long/short value portfolios have similarly underperformed. This has created a similarly rich opportunity.

- Historically, wide spreads have preceded higher-than-average future returns for long/short portfolios.

- Opportunities like this are rare. The last time the opportunity looked similar to now was at the 2000 Dot Com peak. Following on from that peak, value had an unusually strong run from 2000 to 2007.

- The caveat is the 2000 valuations and spread aren’t necessarily the end point. There’s no reason value can’t get cheaper and the spread widen. If that happens, the opportunity continues to improve, but it will underperform while it does so.

- The best returns to value strategies–above-average returns–have all emerged from the times value has underperformed. Now is such a time.

Has value worked?

The value strategy has outperformed over the data we have, with notable periods of underperformance. That proposition has been established many times. See, for two simple graphical examples, the two charts extracted below (from posts on the French data on cash-flow-to-price, and the earnings-to-price).

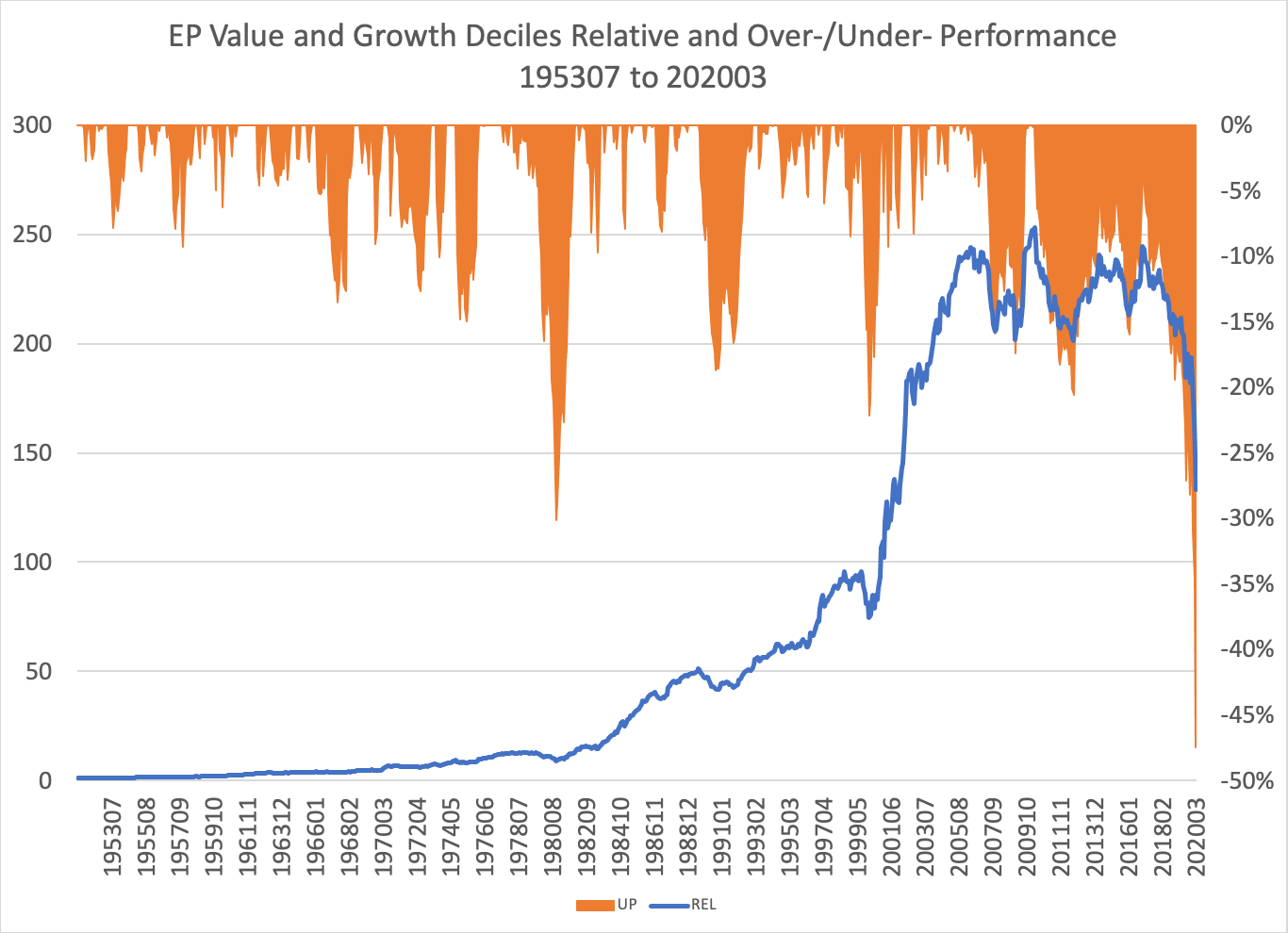

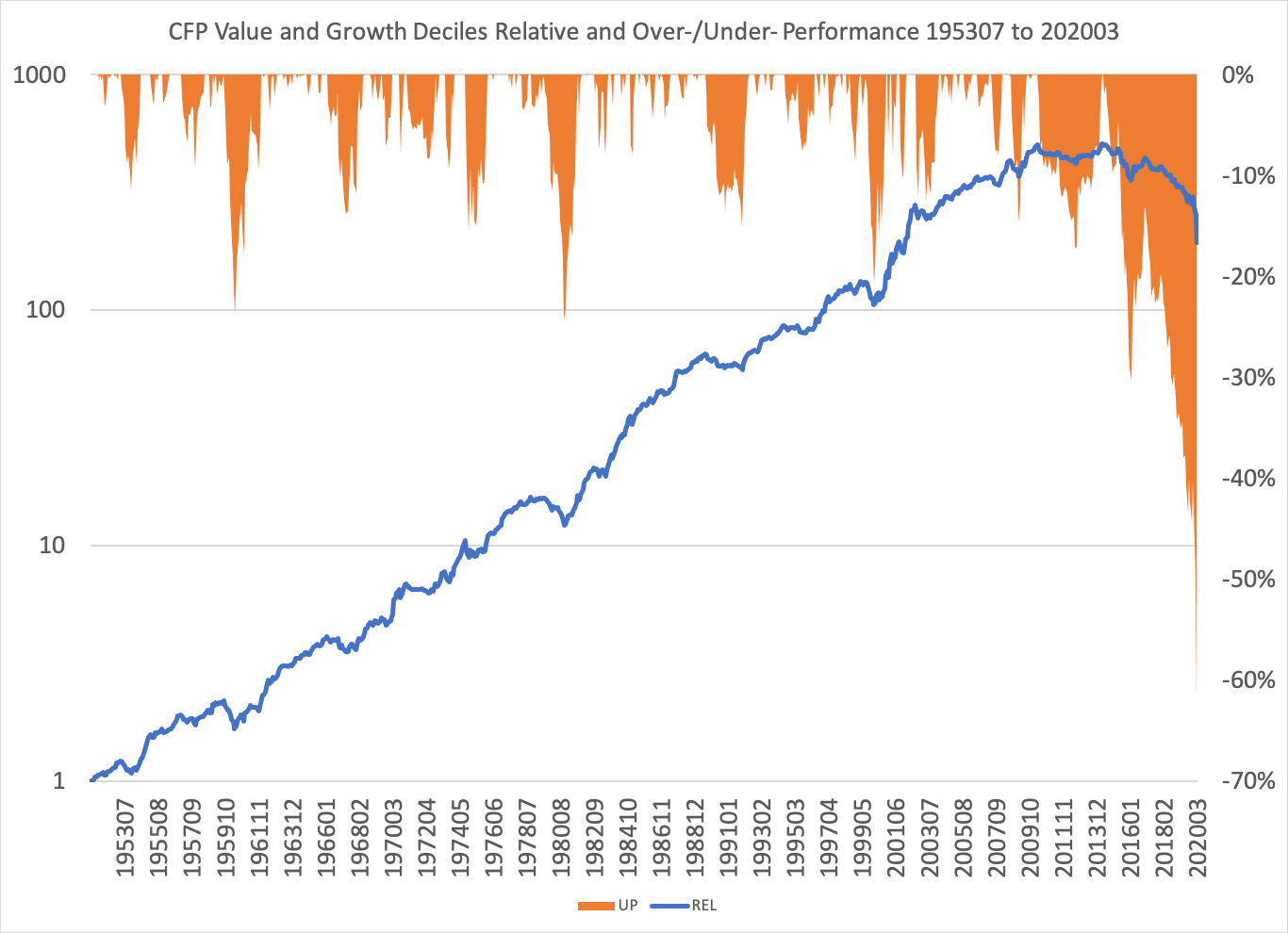

Both value portfolios are still materially ahead of glamour over the full period (relative performance in blue), but the underperformance (in orange) is deep and extended. But value portfolios formed on price-to-earnings stopped outperforming the glamour portfolios in about 2005. Price-to-cash flow value made it to 2014, but has really lost ground since.

French Earnings-to-Price Value / Glamour Deciles 1953 to March 2020

Relative performance (blue, left-hand side) and underperformance from the nearest peak (orange, right-hand side) of equal-weighted decile portfolios formed on price-to-earnings from 1953 to March 2020

French Cash Flow-to-Price Value / Glamour Deciles 1953 to March 2020

Relative performance (blue, left-hand side) and underperformance from the nearest peak (orange, right-hand side) of equal-weighted decile portfolios formed on price-to-earnings from 1953 to March 2020

However it is measured, value is mired in an extended period of underperformance. It has lasted 6-to-10 years to date. Naturally this has led to the question whether the strategy itself will ever work again. Or, in the instance of book value, whether it did in fact work at all. (Yet another example of Sayre’s Law. Corey Hoffstein has a good discussion in Factor Fimbulwinter.)

It’s worth noting that value’s current, extended underperformance, isn’t unique, only rare. In the French earning data, for example, there are many periods of underperformance lasting more than a year : 1953-58, 1963-68, 1971-75, 1979-82, 1989-1992, and 1999-2000. That’s a lot of underperformance. In fact, value underperforms around 70-80 percent of the time. It just does much better when it outperforms. This is the real reason it’s such a difficult strategy to employ. And it’s the reason it continues to work.

Why has value underperformed recently?

The reason value has underperformed recently is because cheap stocks have gotten cheaper. It’s no simpler or complex than that. Prices have fallen relative to fundamentals.

As they have historically, the earnings of the recent portfolios of value stocks continued to deteriorate. The difference this time around has been an absence of multiple expansion, which is the usual case. It is a story of multiple compression, rather than poorer than usual fundamentals. (OSAM discuss this in the same paper above.)

It’s not the fundamentals. Earnings have not deteriorated at an unusually rapid pace. As AQR’s Cliff Asness has shown, stocks in the value portfolios aren’t unusually low earning or levered. It’s multiples all the way down.

As an aside, the designation of stocks as “value” or “growth” usually induces a comment to the effect that “growth is a component of value.” This is true, but unhelpful, and the last time I’ll refer you to Sayre’s Law. The reason for the “growth” appellation is as follows: the high prices paid for the fundamentals of growth companies imply the market expects, all else being equal, higher future growth in those fundamentals relative to other stocks. Empirically, that turns out to be the case–they deliver higher growth (see the OSAM paper). The reverse is true for value. The market expects low or no growth, and value delivers. But it confuses the issue, so I designate stocks with high prices-to-fundamentals “glamour,” and stocks with low prices to fundamentals “value.”

Why is the spread so wide?

The present bifurcation in the market is between high-growth glamour stocks, to which the market has recently been awarding ever higher multiples, and low-, or no-growth value stocks, which are seeing multiples compress. That might sound like the way things ought to be–higher growth should get higher multiples–but, historically, investors have tended to overpay for high growth, starting with multiples that are too high, and been punished with multiple compression. (Similarly, they underpay for the fundamentals of low-, or no-growth value stocks, starting with multiples that are too low, and are rewarded with multiple expansion.) As the OSAM and AQR papers demonstrate, historically, it is unusual that high multiples continue to expand. But that is the case recently.

What has changed over the last 6-to-15 years is that glamour stocks, which have tended to exhibit increasing earnings, and multiple compression, have seen the multiple expansion. And value stocks, uncharacteristically, have endured the compression. An extended period of both multiple expansion and rising earnings has driven glamour stocks to unprecedented levels of overvaluation. And simultaneous multiple compression has seen value stocks fall to rare levels of undervaluation. More on this shortly.

This has created an unusually wide spread in valuation between undervalued stocks and glamour stocks. AQR and Cliff Asness have examined this comprehensively. (There’s really nothing to add to the spread discussion. If, having read Cliff Asness’s paper, you have ongoing concerns about the leverage in the value portfolios, focus on the measures below that use enterprise value, which captures the impact of debt.)

The spread drives returns for long/short portfolios. It’s a useful indicator. In 2014, my Value: After Hours podcast co-host Jake Taylor pointed out in real time the tight value spread had created the worst opportunity set for value in 25 years. Value’s woes since are well documented on this site.

Now, the reverse is true. An extremely wide spread indicates the best opportunity set for long/short value, well, perhaps ever.

The spread is less relevant to long-only value investors. But the news is good there too. As value has underperformed, the long leg of the value portfolio has gotten cheaper.

It would be very bad news if that was not the case because it would mean value has stopped working.

But that is not the case, as we can show below.

Is value cheap?

The charts below show the value decile of various fundamental metrics plotted against their own average. (To eliminate any look-ahead bias in the average, it is calculated as a rolling-average that adds additional data at each point in the series from month-end January 31, 1992 to April 30, 2020.)

When the series is above zero, the metric is rich to its own average to that date. Richer is better. If we assume mean reversion, when the metric is rich to its average it will deliver returns that are higher than its long-run average. The reverse is also true, but, as we’ll see, irrelevant today.

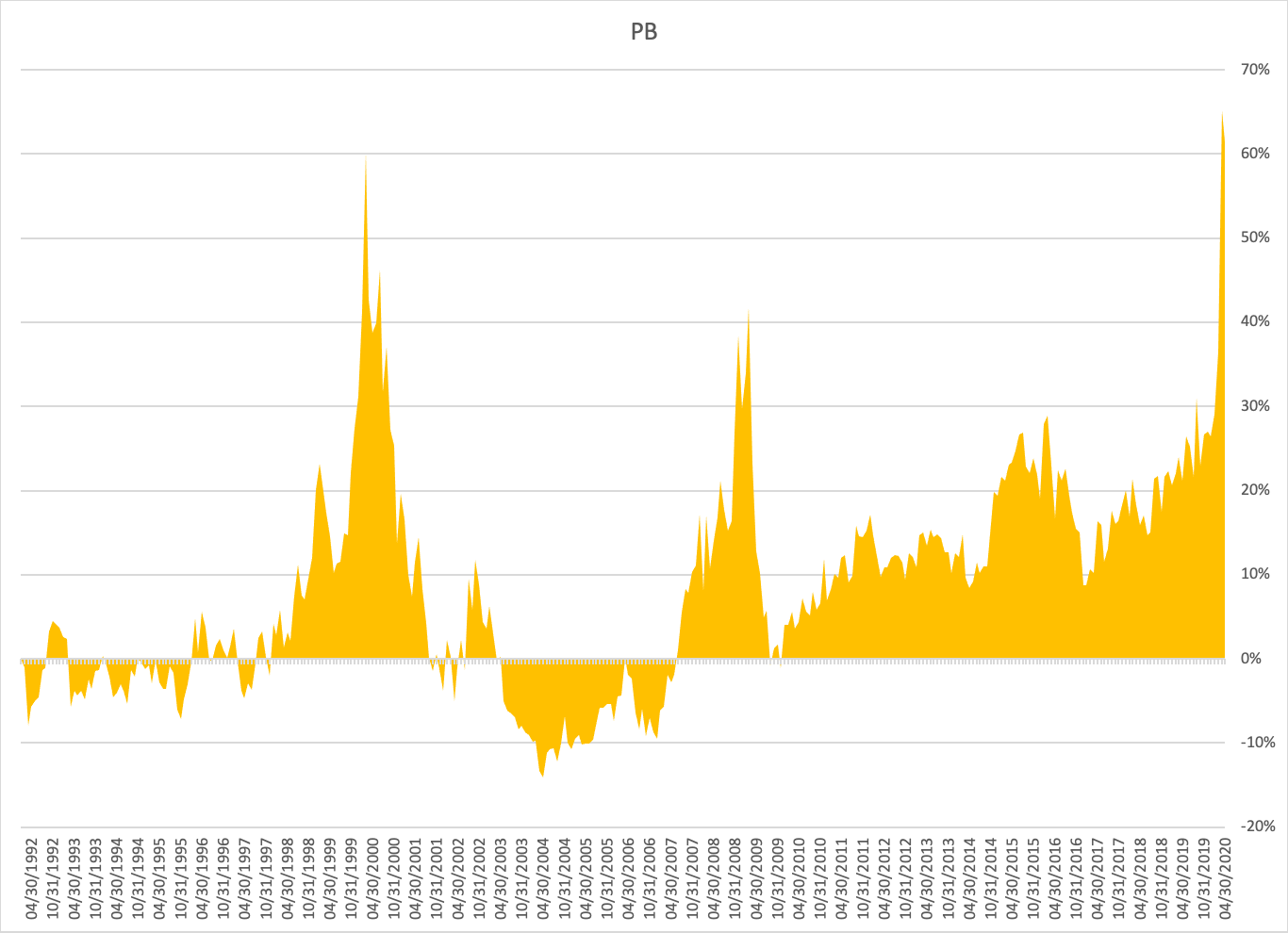

Price-to-book value

Let’s start with the once-and-future king of academic analysis, price-to-book value. Literally, the “value factor.”

The current price-to-book value ratio of stocks in the value decile is 0.23 (BP 4.29), about 60 percent richer than its average of 0.38 (BP 2.66).

The metric has been richer on one other occasion, the penultimate month-end in the data: March 31, 2020.

Whether book value can rise again is open to debate. The issues with book value are well covered elsewhere (see OSAM’s discussion for a good summary). But it’s not possible to rule against it conclusively on the data we have, as Corey Hoffstein’s post demonstrates.

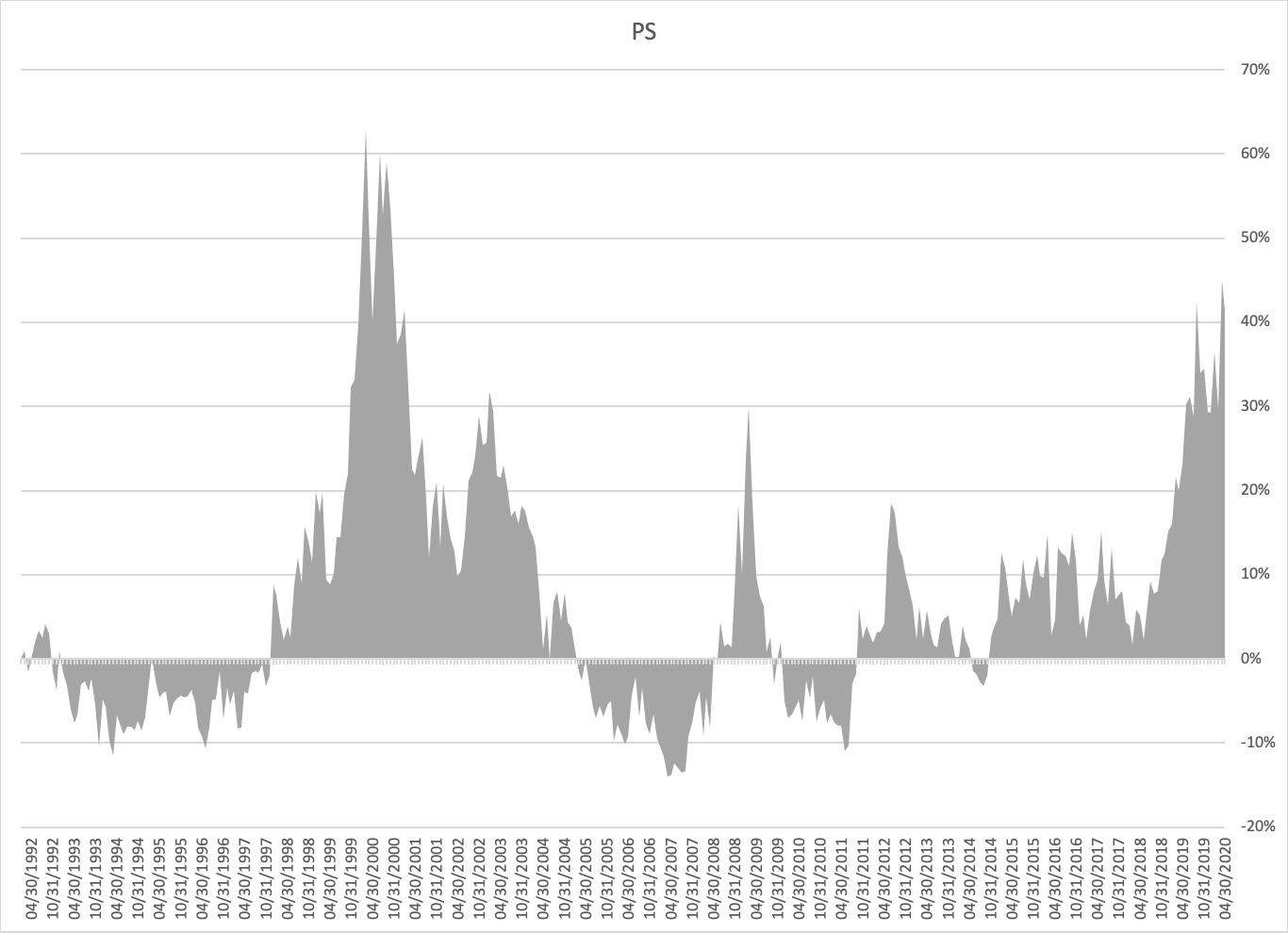

Price-to-sales

Unblemished by all the accounting jiggery-pokery that goes on as we progress down the income statement, price-to-sales is thought to give the cleanest look at the price-to-flows.

The current price-to-sales ratio of stocks in the value decile is 0.14 (SP 7), about 40 percent richer than its average of 0.2 (SP 5).

The metric has been richer on twelve other occasions (fewer than 4 percent of months) in the late 1990s and early 2000s.

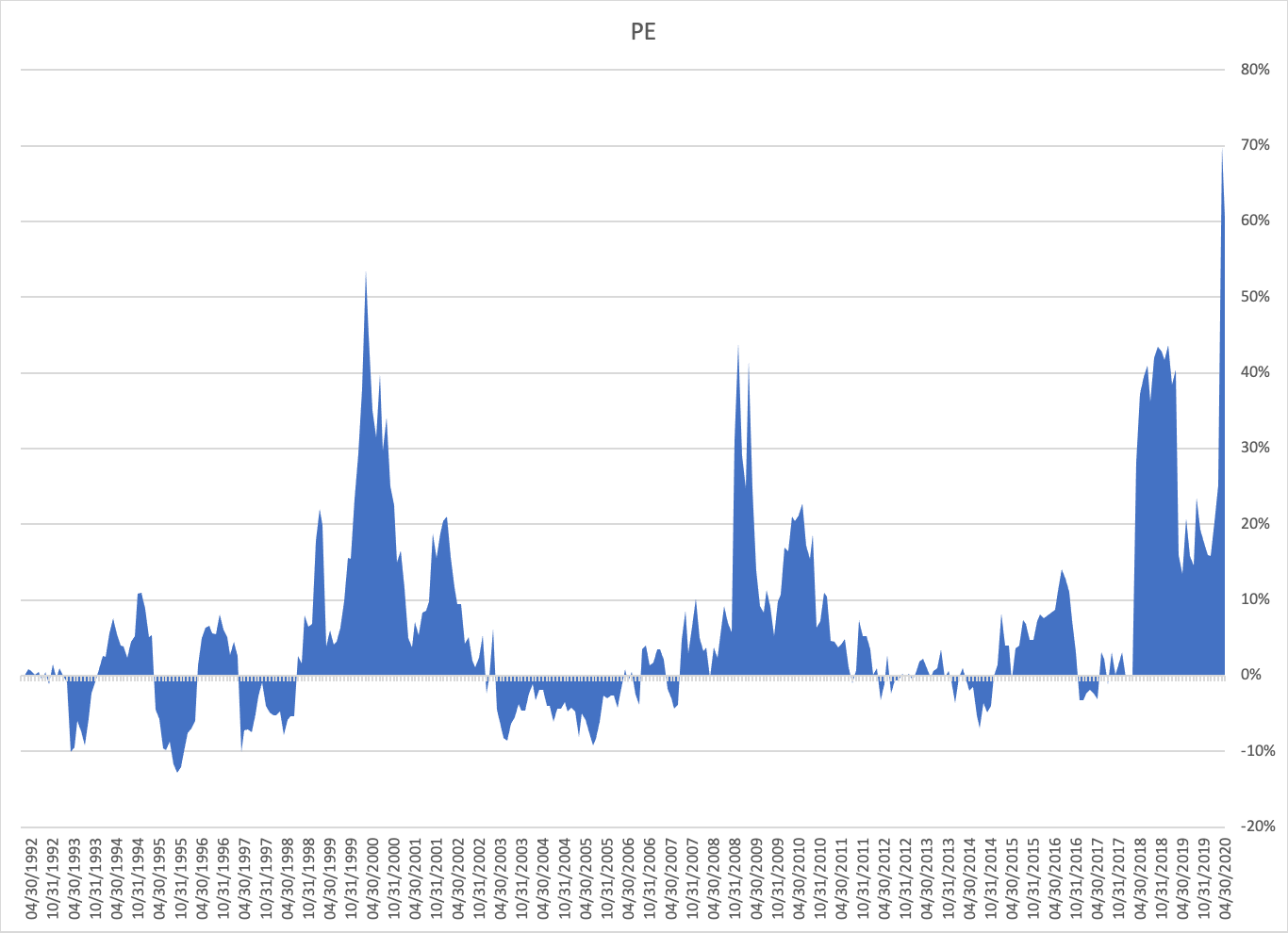

Price-to-earnings

Price-to-earnings shows the price paid for each dollar of profit, the measure that matters.

The current price-to-earnings ratio of stocks in the value decile is 0.25 (EP 3.9), about 60 percent richer than its average of 0.41 (EP 2.4).

The metric has been richer in one other month-end, March 31, 2020.

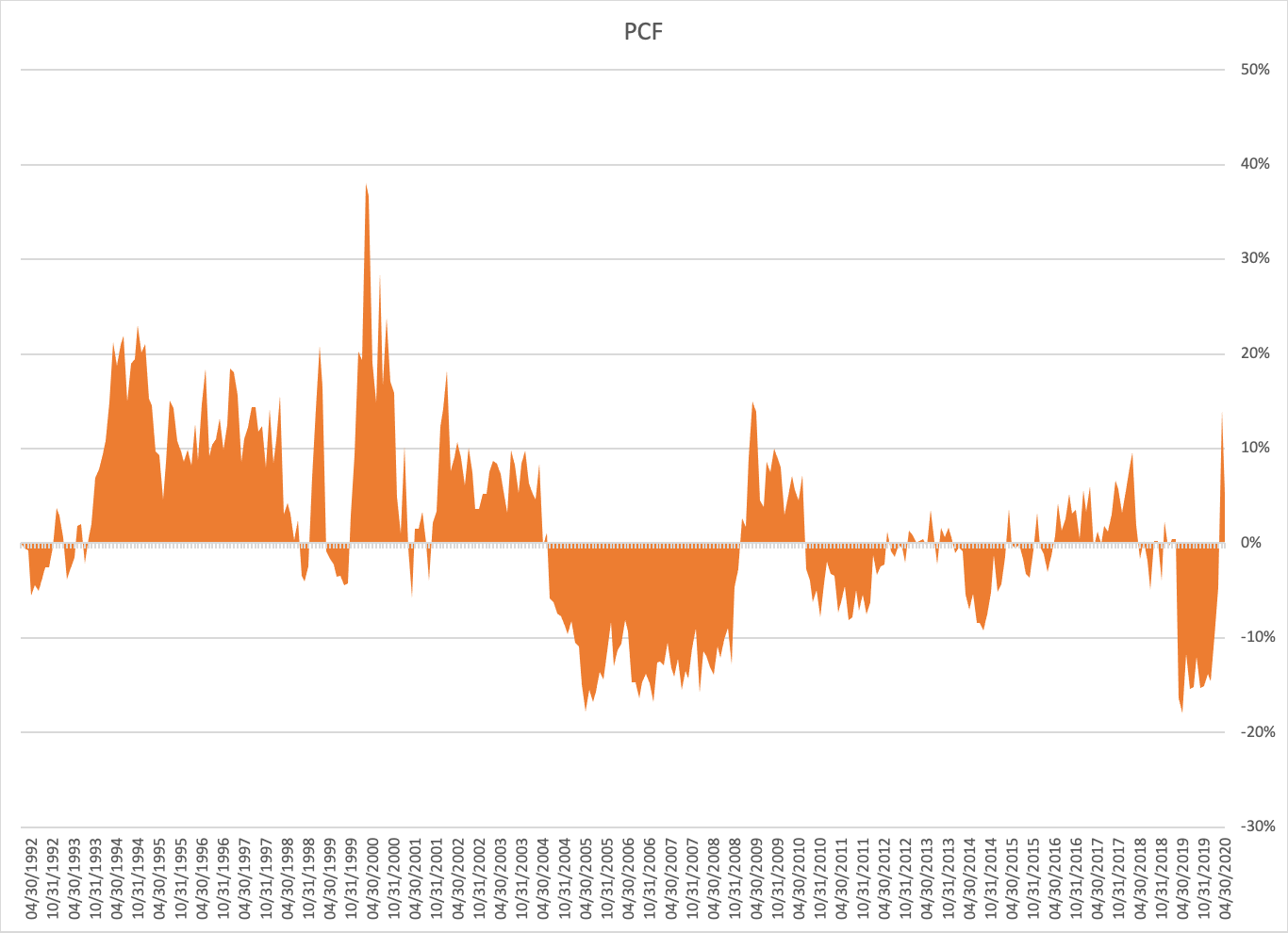

Price-to-cash flow

This is the flow metric that measures what really matters–cash flow–because you can’t eat accounting earnings.

The current price-to-cash flow ratio of stocks in the value decile is 0.2 (CFP 5.03), about 5 percent richer than its average of 0.21 (CFP 4.78).

The metric has been richer almost a third of the months measured in the data series. If you want to challenge the narrative that value is cheap, this is your best bet. Still, value is still cheaper than it’s been about two-thirds of the months in the data set.

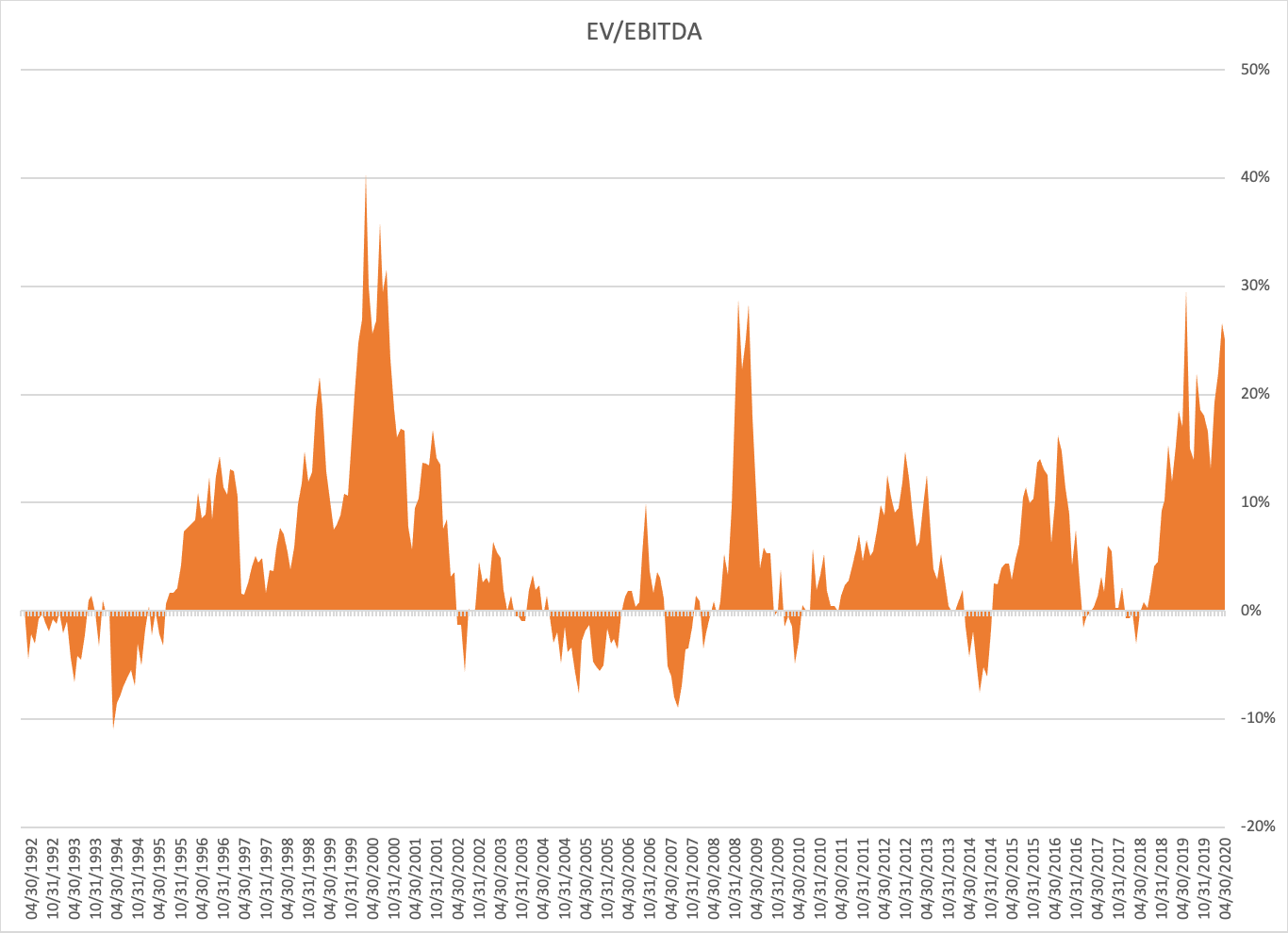

Enterprise value-to-EBITDA

EV-to-EBITDA uses a fuller measure of the price paid, enterprise value, which includes cash, debt and other debt-like liabilities, and compares it EBITDA, a fuller measure of operating earnings. Many value investors prefer the so-called enterprise multiple to price-to-book value.

The current EV-to-EBITDA multiple of stocks in the value decile is 0.47 (EBITDA/EV yield of 266 percent), about 25 percent richer than its average of 0.38 (EBITDA/EV yield of 213 percent).

The metric has been richer on twelve other occasions (fewer than 4 percent of months) at the market troughs in 2000-2001, 2008-2009, late 2018, and March 31, 2020.

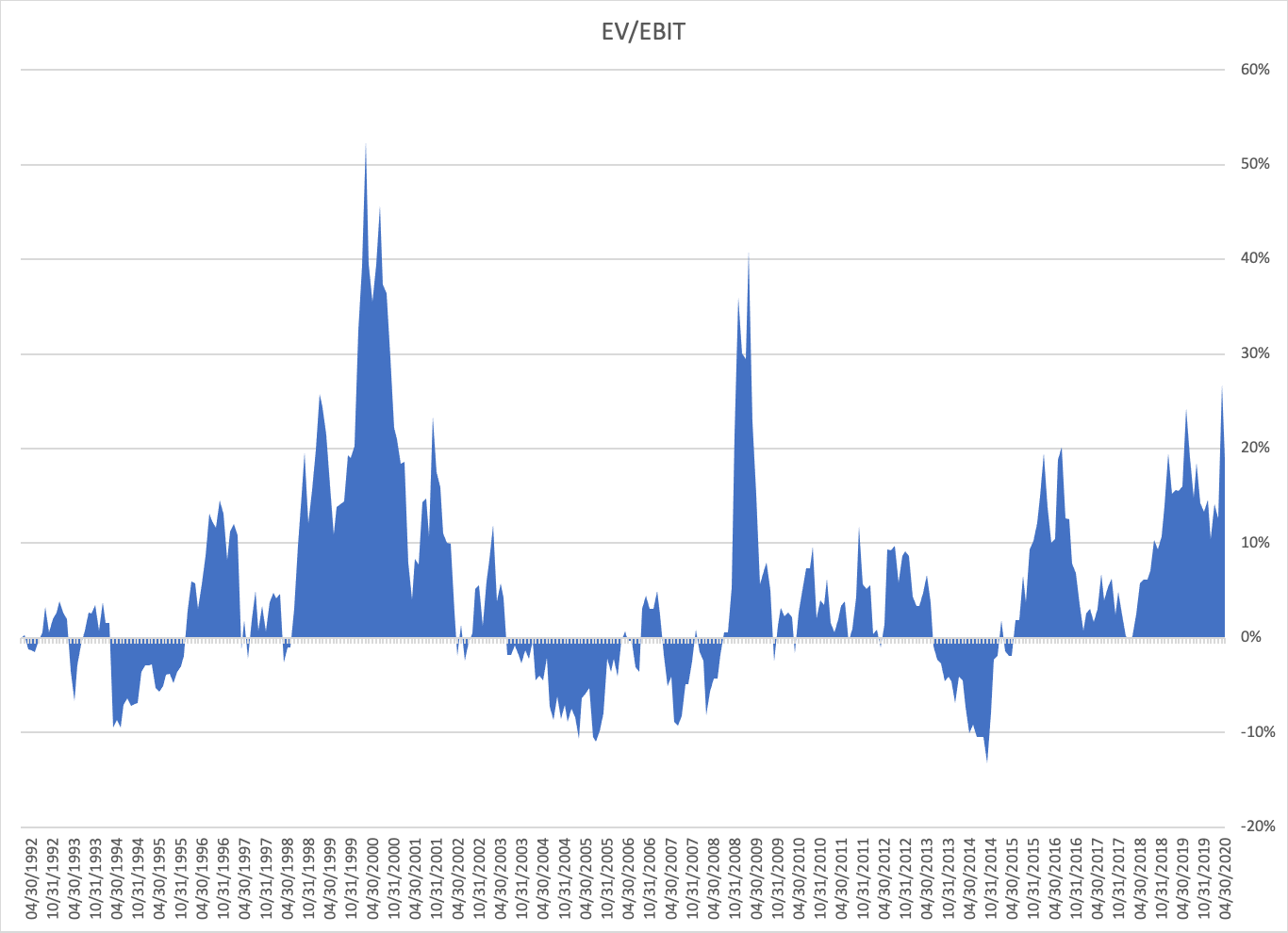

Enterprise value-to-EBIT

Like EV-to-EBITDA, EV-to-EBIT uses enterprise value, and compares it EBIT, an another measure of operating earnings that excludes depreciation and amortization. In Quantitative Value we found this measure to be the one that had performed best over the full data set. This is a close proxy for the acquirer’s multiple.

The current EV-to-EBIT multiple of stocks in this metric’s value decile is 0.46 (EBIT/EV 2.57), about 19 percent richer than its average of 0.46 (EBIT/EV 2.16).

The metric has been richer on twelve other occasions (about 10 percent of months) in 1999-2001, 2008-2009, and March 31, 2020.

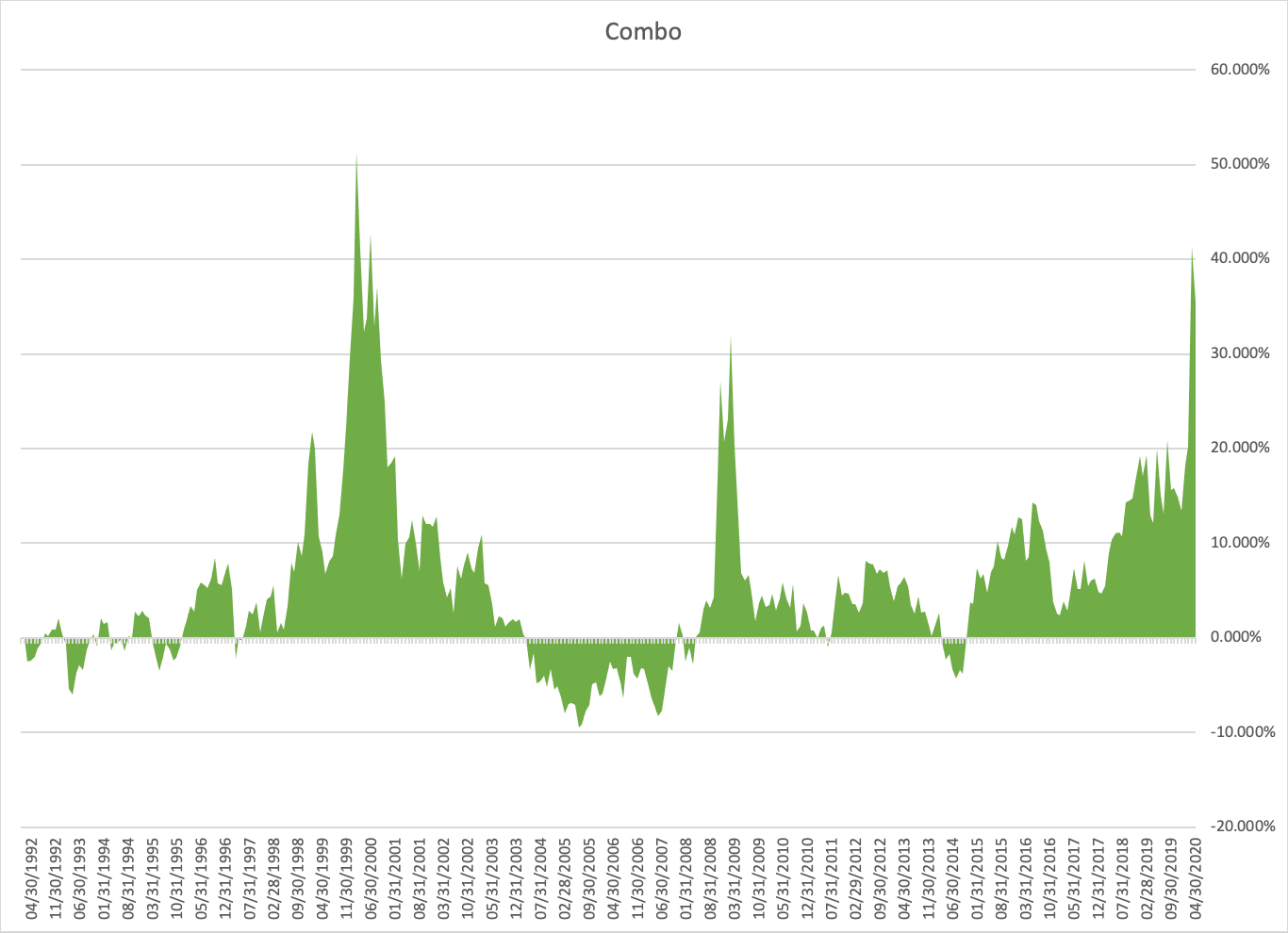

Value Combo

There’s some disagreement between the value metrics above. Book value and earnings suggest value presents an unprecedented opportunity now. Cash flow indicates a good opportunity, but is only about 5 percent rich (still, better than two-thirds of the points in the data series). The others fall somewhere in between. What do the metrics indicate in combination?

We arrive at a “Combo” value score by averaging the scores of each metric scaled to its own average at each point in the data series. The “Combo” value score shows the equally weighted average across all the value metrics above.

The current Combo score of stocks in the value decile is about 35.5 percent richer than its average over the full set.

The metric has been richer on six other occasions (about 2 percent of months): 5 times in 2000, and March 31, 2020, the penultimate month in the data.

The Combo value measure is imperfect, but a better representation than any single metric of the way the average value investor thinks about stocks–not on the basis of any single metric, but by employing a more holistic examination of various fundamentals. Empirically, it renders roughly the same answer many have intuited–that value is currently an unusually good opportunity, and close to, but not better than, the 2000 extreme.

(We could go further, examining the health of the balance sheet, and the business, and most do, but these are properly the province of “quality” factors, and outside this discussion. If you want to see the impact of the full suite of value and quality metrics on the value spread, check out Cliff Asness’s three recent posts on value and the paper.)

Conclusion

Value has underperformed for an extended time. Depending on how it is measured, that underperformance begins in 2005 or 2014. Either way, it’s an unusually long time. But underperformance in value isn’t uncommon. It’s the usual state of affairs.

As long-only value has underperformed, the stocks in value portfolios have gotten richer than usual, and the opportunity has gotten commensurately better. Historically, unusually cheap stocks have been followed by higher than average future returns for long-only portfolios. Value stocks are currently unusually cheap to their own averages.

Over roughly the same time, long/short value portfolios have similarly underperformed. This has created a similarly rich opportunity. Historically, wide spreads have indicated higher than average future returns for long/short portfolios. Long/short value spreads are currently unusually wide.

The value spread is unusually wide, and stocks in the value portfolio are unusually cheap. Opportunities like this one are rare. The last time the opportunity looked similar to now was at the 2000 Dot Com peak. Following on from that peak, value had an unusually strong run from 2000 to 2007.

The caveat is the 2000 valuations and spread aren’t necessarily the end point. There’s no reason value can’t get cheaper and the spread widen. If that happens, the opportunity continues to improve, but it will underperform while it does so.

The challenge for value investors is the best returns to value strategies–above-average returns–have all emerged from the times value has underperformed. Now is such a time. Hold hard.

Data Source: Ken French’s Data Library and Alpha Architect’s Visual Factors page. The analysis is mine.

For all the latest news and podcasts, join our free newsletter here.

Don’t forget to check out our FREE Large Cap 1000 – Stock Screener, here at The Acquirer’s Multiple:

5 Comments on “Is value a value trap?”

Im inspired to hodl on value! Here are two thoughts that lit up during the reading of this blog.

1) The underlying unit of accounting (USD) doesn’t matter anymore, so all that is important is the business, what it does, and how society “values” it. At least that is what it feels like in this tech 2.0 bubble.

2) Is there a correlation between wealth inequality and the spread between value and growth stocks? I’m just curious.

This really does feel like tech bubble V2.0 plus monetary system collapse all rolled into one. My question more than anything is what does our society value? I think thats where the real battle ground is, should we work “hard” for money and find “value”, or can we simply rely on technology to get us out of this “work hard for money” idea.

Thanks Saam. Great point and question. I don’t know the answer. I do think pinning interest rates down punishes value and inflates glamour because of the difference in duration in the return streams (value is front-end loaded and expected to diminish over time, glamour is back-end loaded and expected to grow. If you model that in a DCF and change the rate assumptions you’ll see glamour is more sensitive to the rate).

Interesting point, I have not thought of that! Thank you.

Great piece. However, I am not sure that this is the right way to think about. Value works because of the re-rating process (multiple expansion of depressed multiples). It does not work if the re-rating process does not happen.

Will the re-rating happen? I don’t know. But it does not suprise me that the spread between stocks that will suffer from the biggest depression in 90 years and those that will benefit from it, is at record high. It should be. It is reasonable for it to be this way.

What I wanted to say is: Relevant is whether the re-rating happens. Re-rating happens when earnings detoriate less than expected.

Oppertunity exists when stocks are rated unrational low compared to rational future expectation.

In this kind of thinking the spread plays less of a role. The question is not so much how big is the spread but what does the future hold for the cheap companies and the expensive companies. Backtests will not give an answer to that. A theory potentially can.

Wide spread causes big future returns is a solid theory. Unrational low expectation of future earnings causes big future returns, might be a slightly better theory in my opinion.

What about mean reversion as a theory? Tricky. It either postulates randomnes in the system or a mean reverting cybernetic process. Whether this really exists and whether it is causal for something needs to be discussed more deeply.

I hope this makes my point more clear.

Are the cheap companies rated unrational cheap? Are the expensive stocks too expensive? I am not sure in the corona recession.